|

| Cloud, Digital, SaaS, Enterprise 2.0, Enterprise Software, CIO, Social Media, Mobility, Trends, Markets, Thoughts, Technologies, Outsourcing |

ContactContact Me:sadagopan@gmail.com Linkedin Facebook Twitter Google Profile SearchResources

LabelsArchives

|

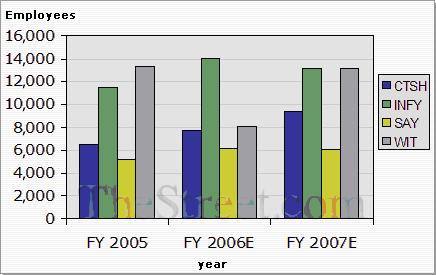

Saturday, December 31, 2005Bidding Goodbye To Microsoft Monopoly Between Jan 1 2005 & Jan 1 2006, Microsoft appears less and less powerful - hardly looks like the tiger getting stronger - but looks increasingly challenged on several fronts. Slashdot's Roblimo has written an interesting essay titled - Is Microsoft Still a Monopoly?. He writes,"Microsoft Windows still dominates the desktop. But in many other areas, including Web servers and supercomputing, Microsoft is just one player among many, and often a weak player at that. On the gaming side, despite the latest xBox getting all kinds of media buzz as "the" console to buy, Sony's Playstation outsells the xBox at least two to one, and many analysts expect Sony to widen that gap even more when Playstation 3 comes out in the Spring of 2006. On the Internet, MSN and MSN Search are so far behind AOL and Google that it isn't funny. And even on the desktop, Linux keeps getting stronger, while Mac OS X is commonly accepted as more reliable, secure, and user-oriented than Windows. He has assessed various factors that are making Microsoft dance and concludes that - “No matter what Microsoft does, it will never have a software monopoly again. Nor will any other company". The barriers to entry in the software business have become too low for that to happen, and too many skilled software developers are learning that they can earn at least as much working for themselves as they would by working for big software companies”. Category :Microsoft, Opensource, Emerging Trends. | Online Intersections With Traditional Media USA Today ran a story about U.S. music album sales. Get this: 2005 album sales were down 7% from the previous year while digital downloads of music doubled! U.S. album sales were down about 7% as 2005 drew to a close, but the budding market for music downloads, which more than doubled over last year, helped narrow the revenue gap. The article goes on to note that this isn’t particularly bad news for recording companies, but “it doesn’t bode well for music retailers.” Combined, album and singles sales fell about 8% over the same time last year. More than 95% of music is sold in CD format. Downloaded tracks from online retailers soared to 332.7 million this year, compared with 134.2 million in 2004, an increase of 148%. Download sales increased by 350% over the prior year. Michael Hyatt predicts, a big enough slice of the book reading public will opt for digital delivery and that will have a significant, disruptive effect on the entire industry. As he sees it, 5-10 percent reduction in sales would wreak havoc. It’s already happening with newspapers and magazines. On the other hand, publishing companies that anticipate this shift and prepare accordingly will prosper.He is spot on when he sees that when technology shifts happen – quality does not matter beyond a certain level - The quality of MP3 files is not as good as the quality of CD tracks. Yet, customers are switching in unprecedented numbers. The trend of having 10,000 songs at your fingertips in a device that can fit in your pocket is intoxicating—at least to millions of people. Category : Emerging Trends, Disruptive Technologies, Online Strategies | Steve McConnell : Good Read Steve McConnell is one of my all time favourites – in fact he distills rich experience into very well articulated set of advise – I keep telling all software developers that all Steve McConnell’s writings are a must read – I think that he has the right flavour and mix in discussing various software engineering concepts – all embellished in simple, direct and practical terms. So when I came across the online version of his classic mistakes enumerated, I can not resist making mention about it here. Here are some types of the 36 classic mistakes that McConnell describes in detail: Category :Favourites | Friday, December 30, 2005Web 2.0 : Time For A Reality CheckWeb 2.0 is clearly getting disproportionate coverage in the blogosphere. Web2.0 share in the real world as delivering value to business and society is indeed limited - if we look at the enterprise software – they directly are responsible for making the business machines hum and improve- be it airline scheduling, dispatching crude oil or treasury management or powering the stock exchanges of the world. Mike Arrington lists out a set of Web 2.0 applications that he sees as quite essential – the list has within it - some well known names – Technorati,FeedBurner, Bloglines, Flickr, Memeorandum, del.icio.us, skype & WordPress etc. The enthusiasm and the excitement shown for Web 2.0 apps amazes me – as these defy long held priniciples of wisdom. Its high time that these so called Web 2.0 companies are examined from the first principles viz. Business models – merely becoming attractive to be bought over by Yahoo’s & Google’s of the world would not be sufficient. If you see closely even the valuations of bought out firms have been very moderate.No doubt advances in technology to develop and distributed services off the web is an important landmark – most of Web 2.0 apps germinate out of this. The reigning mantra seems to be - "build it first and figure out how to attract visitors – they will anyway come” business model – the underpinning hope is that once a critical mass of visitors are achieved, revenues can always be generated. AdSense funds the operational cost of several web 2.0 enterprises. Surely not the way to build a scalable & enduring business . I sort of agree with the view web 2.0 lacks meaning & magic. I am fine with already established players like Amazon & Google getting web2.0 tagged – am also fine with finding a productive niche to thrive in the information value chain. Moving forward like in the e-business space, we need to have the wisdom and mechanisms for cross-integrating/leveraging web 2.0 applications for larger benefits – this calls for standards in development , build & integration blocks – all this would come only out of a solid base of web 2.0 apps that get built beneath – truly a tall order given the fragile nature of several web2.0 entities. We can definitely see a petering out of the web 2.0 momentum as we see it now and several entities would disappear – but one hope is that out of this something robust and strong might emerge – but we have cut through the hype. Category :Web 2.0, Emerging Trends, Emerging Technologies | Offshoring IT Services : Signals Getting Stronger Ronna Abramson finds that an increasingly huge pool of global demand makes it a good bet for India's top IT outsourcing firms to outrun their larger rivals in 2006. The year ending Mar 2006 will mark a milestone for Indian offshore outsourcing firms - Infosys and Wipro, as their revenue crosses the $2 billion mark. Satyam has already crossed the billion dollar run rate this year. The Fortune 500 Blogging IndexChris Anderson writes about a wiki created collaboratively developed together by between Socialtext & Wired magazine that tracks which of the Fortune 500 is blogging. The list finds that only 3% of the F500 are doing so. Microsoft blogs, and Apple doesn't. Sun blogs and Intel doesn't. GM blogs and Toyota doesn't. In a meeting with Doc.Searls the question arose and Chris writes in the eyes of Doc - the risks and uncertainties of public business blogging are so great that big companies only do it under duress, when their traditional corporate messaging has lost traction. So companies on the way up don't want to mess with their success by introducing a new lens on the enterprise that isn't controlled by the PR department. But companies on the way down are willing to try anything to regain the confidence of their customers.This site has a list of F500 companies with blogs – both internal and external are listed here. The NewPRwiki also has a list of CEO blogs. This spreadsheet lists the Fortune 500 blogs & he finds that the average trailing 12-month share performance of the blogging members was +5.7%, while the non-blogging members was +19%. A commendable effort in compiling the list. This Fortune 500 Business Blogging Wikiis created to expand the list. Somehow I could not find in the excel sheet - noteworthy IBM blogs from the likes of Irving Wladawsky-Berger, Amy Wohl, Grady Booch and countless others from the IBM stable.what may be seen as extending things too far, Chris says the idea is to make the list robust enough to create a business blogging index!!! Category :Blogs, Emerging Trends | Thursday, December 29, 2005Morgan Stanley on Outlook for India -2006While it is fashionable to be bullish about the growth of Key countries in Asia, Morgan Stanley takes a cautious view about the outlook for India in 2006. An acceleration in GDP growth over the last two years to 7% pa has been one of the key factors focusing investors’ attention on India. Although we have been positive on India’s long-term growth outlook, we believe that the recent acceleration in growth was driven largely by cyclical external stimulus. Given that these favourable global factors now appear to be reversing, we believe India will face a pullback over the next 12 months in the form of a slowdown in growth and tightening liquidity conditions. A large part of the recent growth in industrial production and to a lesser extent services sector growth has been driven by cyclical global factors. This strong global liquidity spillover into India has allowed the government to pursue relatively loose monetary and fiscal policy, pushing domestic consumption growth to a new high. Acceleration in consumption growth has largely been driven by a rise in borrowing rather than income growth. India’s share of goods exports to the US has not seen any significant improvement over the past two years, and therefore most of the acceleration in India’s export growth appears to be largely a reflection of the demand cycle - this is important as asian economies are in general dependent on exports to US.The report also says china is about to suffer from an export fatigue. Although the Indian economy continues to benefit from relatively low global interest rates and stronger global GDP growth, the government has cushioned the economy from the attendant cost of higher oil prices. Category :India, 2006 Outlook | Enterprise Predictions for 2006 These are the comments that I posted in Vinnie’s site upon seeing his 2006 enterprise software predictions. In general, buyers are more cautious and would not easily get sucked in vendor speak – lot more detailed evaluations and price negotiations, clarifications can be expected – the average sales cycle may also increase for enterprise players – not shorten as expected due to consolidation effects. Category :Tech Predictions 2006 | Alaska Airlines #536 - Anxious MomentsJeremy Hermanns, a passenger in the Alaska airlines flight bound for Burbank, and a GA-VFR pilot, writes about the Alaska Airlines cabin depressurization and panic at 30000 feet. Seattlepi reports that an aviation expert finds that the jet was probably struck by a baggage cart while at Sea-Tac and the incident was not reported before the plane took off for Burbank. The damaged area of the plane would have been weakened by the ramp incident and the aluminum skin then likely ruptured once the jet neared its cruising altitude. All this happened due to a non-unionised member probably damaging the fuselage!. Oh God.. Now I realize how valuable the words - "travel safely" and "happy landing" means. I did not see any press release in Alaska airlines website on this incident. Look at the saftey numbers and also this impressive document on safety fromBoeing.Also good to know that no one was injured in this - aviation safety, is in many ways an important driver for global economic engine to keep humming - the more and more that we can make it safe - all the more better. Category :Aviation Safety | Wednesday, December 28, 2005Microsoft : Looming Challenges AheadWhile some beleive that Micosoft shall have a good year ahead, Ray Ozzie's perspective about what microsoft could be doing in the year ahead - there are some important area where Microsoft's progress shall be monitored in the coming year.This list provides a good summary of key themes that Microsoft needs to go after in the new year.Besides taking Vista to the boardroom- microsoft needs refresh its online strategy. Itslatest online strategy is to match Google’s every move in hopes of raking in more advertising dollars, while taking yet another stab at subscription services. 2005 saw a lot of motion—leaked memos, blog buzz, reorgs, and a new "Live" brand—but little progress in terms of service improvements, audience share, or dollars. I agree that Microsoft’s online strategy must start to gel in 2006, or the company will find Google continuing to steal headlines and rake in the advertising bucks—or worse, building online services that begin to compete with Microsoft's core software franchises. Category :Microsoft | Korea & ConvergenceJapan and Korea have always been the trendsetters in the mobile and convergence segments. Korea'sbroadband advances are amongst the most recognised about the nation. Courtesy of Smartmobs saw this assessment of the status of convergence in the Korean market. I had been to Korea several times and in many ways associated with several developments there – and it is interesting to note that indeed the telecom market was dominated by Category :Convergence, Korea | The Rise Of KPOSeveral months back I wrote,Every form of digital data – creation, transformation and reporting is up for grabs in the offshoring world. Eric Keller was indeed right when he wrote, took Japan more than 30 years to obtain a strong position in key U.S. industries, such as Automotive and Consumer Electronics and that It will take half as long for India to do the same for service-oriented industries with IT leading the charge. Britton now writes, "Get Ready for Knowledge Process Outsourcing". As he sees it, the next wave of offshore outsourcing will revolve around high-end knowledge work. It may also have important implications for companies engaged in customer analysis and intelligence initiatives. Category :Knowledge Process Outsourcing | Portals To Choose Insurance AdvisorsWe have so far seen chat being used interactively for customer services - online customer interaction has never really gone beyond in a sustained way.Just as internet banking empowered customers online shopping experience, Insurance companies are trying to innovatively make use of the internet and collaborative platforms to provide better interaction experience with the customers. ING Vysya Life has borrowed the blogging concept to provide an online presence to its top insurance advisors who can use the portal to increase their strike rate for converting their business from a larger number of potential customers. The platform provides the prospective customers the facility to select from the 27 advisors in six cities featured on its Web site and interact with them to get comprehensive information on insurance products. The interactive service will not eliminate personal meeting to clinch the subscription but is aimed at helping in sharper advisory capabilities to target the right products to the right customers. ING maintains that this service could be scaled up globally if found successful. . This is quite noteworthy. I would typically like to see the kind of tracking that the fedex uses to trace status - ideally service companies should be in a position to track and expose progress of the movement within the department to let stakeholders know about the progress. This should happen eventually. |Paul Graham On Time Management & Procrastrination Several people ask me repeatedly , how I manage things amidst so much of travel. I do not know whether I am all that good in managing things in time – most of my friends think that I can do better!! However I see some colleagues who do much better on this front – with so much travel they accomplish a lot more.Time management doesn't begin with managing time, it begins with finding our own individual purpose, establishing our mission, and setting our goals to achieve that mission. Paul Graham, points out that there are three variants of procrastination, depending on what you do instead of working on something: you could work on (a) nothing, (b) something less important, or (c) something more important. That last type, is good procrastination. Type-C procrastinators - put off working on small stuff to work on big stuff. Good procrastination is avoiding errands to do real work. The mildest seeming people, if they want to do real work, all have a certain degree of ruthlessness when it comes to avoiding errands. The reason it pays to put off even those errands is that real work needs two things errands don't: big chunks of time, and the right mood. If inspired by some project, it can be a net win to blow off everything else to work on this for the next few days to work on it. Yes, those errands may cost more time when you finally get around to them. But if a lot get done during those few days, you will be net more productive. In fact, it may not be a difference in degree, but a difference in kind. There may be types of work that can only be done in long, uninterrupted stretches, when inspiration hits, rather than dutifully in scheduled little slices. Conversely, forcing someone to perform errands synchronously is bound to limit their productivity. The cost of an interruption is not just the time it takes, but that it breaks the time on either side in half. Years back Steven covey’s book First things first defined a minor framework – to classify criticality of time management Category :Time Management ,Life Trends | Tuesday, December 27, 20052005 : The Year Of Google As the year comes to an end - amongst several enterprises that made news for the moves made - Google stands out - one gets a felling as if the year thats about to end should be christened THE YEAR OF GOOGLE.The Google of yesterday is different from the Google of today and with several new initiatives like this – and moreover there are several initiatives - some known, most unknown, the Google of tomorrow looks more interesting. Some see google as privacy time bomb, some see it as an evil and some hold even more radical views about Google. This post captures all the Category :Google, Emerging Trends | Mark Fletcher, Bloglines & Blogworld Mark Fletcher,who earlier wrote about his experience in starting Bloglines – one of the most notable success in the blogworld – real startup, garage mindset & launched with the philosophy to keep things simple but allow for scaleup is indeed a phenomenon in the blogosphere. His presentation on bloglines startup experience is a must read for all those interested in entrepreneurism and the evolution of the blogosphere. Mark and Bloglines are clrear trendsetters and consistent winners - even after Askjeeves acquisition,it is really an achievement of sorts to have retained the old look and feel and maintain the same user experience . Mark writes about his experience in moving bloglines infrastructure recently – aimed at moving the Bloglines service to the main Ask facility, as it would be easier for operations, it would be easier for to quickly expand in the future, and it would be easier to tie into other parts of Ask Jeeves. Category :Bloglines, Interesting Technologies | Monday, December 26, 2005Indian IT Labour ShortageA McKinsey -Nasscom study finds,If India doesn't take urgent action to reform education and build modern infrastructure, the nation could fall far short of its potential as an outsourcing haven. The first inklings of a tightening talent supply are already visible in rising staff turnover and skyrocketing wages. If offshore outsourcing work grows as rapidly as expected, the study predicts, in five years India will have a shortfall of 150,000 IT engineers and 350,000 business-process staff. Software houses shall have to face this problem in several ways - that may include leser margins as well.The problem is not non -fixable - with concerted efforts from Government, educational instituitions & corporates - Read the specific recommendations( thought they look geneic - the roots of the solutions anyway lay there) to overcome the shortfall and once can easily relate how this fully doable. Am uplodaing from airport and hence very brief - shall write on this is in detail a litte later Category :India | Open Source : Outstanding Issues GaloreSeveral months back,while writing a brief note, on opensource, I concluded that that from a technology, economic and sociological perspective, there is no compelling reason for the open source model to succeed and become dominant. We can assume at best - a niche role for open source in the IT industry. A few months later, I wrote opensource is not yet ready for the enterprise and pointed out that I tend to take a dim view of open source relevance - see Open source -where is the business model, Opensource : Costly & Litigatious and also covered Kim Polese view business models of the open source support companies – where the contours of what need to be done to support open source components become quite clear and a not seeing several players in the opensource world thinking along these lines – it would be a major impediment to consider adoption of opensource in enterprises if the support model is not made widely available and the economics and technology upgrade rate demonstrated as beneficial. I also recently wrote about FOSS movement winning the hearts & minds of the Indian programmer & highlighted the need to have a robust instituitional and infrastructural support for the movement to gain support from offshore developers. James McGovern is urging opensource analysts to provide details of talent search mechanisms, non-technology corporates interest in opensource, vertical solutions using opensource solutions, details of opensource competing and winning against commercial software, best practices in opensource contributions and the like. Look carefully at the set of issues that he has raised – very essential to build up any movement – daring to challenge well established notions of software – Like James , I shall await for pointed responses to these.( Disclosure – Have tried in the past – with limited/no success to get such specific, credible details). Category :Open Source | Blogherald's Blogosphere WatchAlong with the observation that Time has dropped Blogs of the year award this time around, ( it is becoming a little difficult - we need to admit given the huge explosion of the blog population and the cacophony of voices and the various themes around which ideas are expressed.)Blogherals publishes the list of top ten interesting people in the blogosphere. Among the ten, I certainly find these four very interesting. Category :Blogs | The Internet Explosion & Changing DynamicsTen years ago, the net was mostly used by geeks; now it's the default way to do business in many countries. Some time in 2005, a dramatic milestone was reached in Internet history: the one-billionth user went online. Because we have no central register of Internet users, we don't know who that user was, or when he or she first logged on. Statistically, we're likely talking about a 24-year-old woman in Shanghai. Morgan Stanley estimates, 36% of Internet users are now in Asia and 24% are in Europe. Only 23% of users are in North America. Om Malik was amongst the first to talk about this. Jakob Nielson points out that it took 36 years for the Internet to get its first billion users. The second billion will probably be added by 2015; most of these new users will be in Asia (The clickz report finds that this can happen much earlier – it talks about adding another 750 million people by 2101). The third billion will be harder, and might not be reached until 2040. Jakob predicts that e-commerce sales will at least double from their current level when more of the current billion users start shopping online. We previously noted that online monetization continues to rise. Jakob Nielson highlights some key things to note amidst this growth: The billion-user Internet is a highly diverse environment that has moved far beyond the elite in Silicon Valley and other global technology hubs. There are hundreds of millions of old people online, and there are even more users without fancy graduate degrees. The difference between elite and mainstream users is getting bigger every day. In another ten years, Americans will be less than 15% of Internet users and will likely account for about one-third its value (Americans typically spend more than other users). The fact that two-thirds of Internet revenues will come from other countries highlights the growing importance of global reach of the internet.Putting aside the details of how to make the multi-billion-user Web work, the very fact that it's realistic to expect a second billion users points to interactive media's compelling value. People all over the world are experiencing unprecedented levels of empowerment: being able to do things is why the Web has grown so fast, and will continue to grow for years to come. Category :Internet, Emerging Trends | Technology, Internet & Aviation IndustryAirlines, Internet & New Economics is an interesting area to watch. Around the world airlines are trying in different ways to make the internet work for them. Electronic ticketing now accounts for 38 percent of tickets sold worldwide and IATA wants the 265 airlines under its wing to achieve 100 percent paperless ticketing within two years. IATA says that there are roughly 350 million tickets printed annually. By 2007, IATA believes that paper tickets may not be needed any more. The benefit – estimated annual savings of three-billion-dollars for the industry, while wider use of new electronic technologies for self service check-in, luggage handling and freight could offer even more in years to come. The beauty is this is not a revolutionary technology but this promises savings and improved convenience all the way down the line to the passenger.The arrival of the Internet booking engine gave self service centre stage in the travel industry besides rediced fares. From 40 million people users of internet in 1995, last year there were an estimated 870 million Internet users, according to the International Telecommunications Union. About 400 million travellers are expected to book online direct with airlines in 2005 - the Internet has also changed the operating environment for established airlines. Across the world, the adoption is showing huge progress. In countries like India, 25% Of Travel Business get done through the internet. Budget airlines by embracing e-ticket initially scored over mainstream competitors .The Internet has helped drive down airlines' costs but it has also fuelled price competition, damaged yields, and exposed the weakness in legacy computer systems in supporting pricing and increasingly complex distribution channels. The industry is scurrying to secure other types of electronic gadgetry to speed progress - and cut costs - on the ground. After the introduction of electronic check-in kiosks by some airlines, moves are now afoot to establish a common technical standard that will allow airports to install the same self-service equipment for all. The Internet is also allowing the development of check-in from home, which is expected to emerge in 2006. Passengers are promised "flash bag drops", stress-free travel and less queues on their way to their flight, while radio frequency electronic tags - RFID - could cut down on lost luggage. As we noted earlier, the rise of the ATK says far less about ruthless “reductions in force” and more about airlines’ desires to mass-produce just-in-time convenience. The traveler experience is getting more and more attention - While inside airports travellers need not think. Mindlessness is a mantra for every Executive Platinum flier.. Continental Airlines’ mean time for automated check-in is 66 seconds. You only have carry-on bags? Barely 30 seconds.As a promoter of mindlessness, the ticketing kiosk’s superi¬ority to the ATM is obvious. With an ATM, you think about how much money you need and how much you actually have. In contrast, an ATK (airline ticketing kiosk) presents you with choices you either have already made (your itinerary) or don’t need to think about (are you carrying any firearms onto your flight?). In all next the internet’s reach to commoners are best exemplified by its leverage by the aviation industry – but the key thing to watch is – more and more of these are all set to happen. Category :Internet, Airlines + Technology, Emerging Trends, Emerging Technologies | Sunday, December 25, 2005Amazing Amazon.com & Its Process EdgeThink technology & holiday season, Amazon has top of the mind recall. With its unmatchable process edge, Amazon.com seeks to be Earth's most customer-centric company, where customers can find and discover anything they might want to buy online, and endeavors to offer its customers the lowest possible prices. (Image courtesy : Businessweek) Category :Amazing Amazon | RSS Reader Becoming Integral Part of Outlook Bill Burnham once wrote that in the contest between E-mail & RSS,the former easily wins. Addressing the blogger’s constituency, he added that given the almost ubiquitous reach of e-mail and its "push" nature, for reaching users, one should probably make e-mail the preferred means of subscribing to any blog. Sometime back Microsoft announced that it is baking RSS into Vista – at the platform level itself. Microsoft’s belief is that RSS is so powerful that it needs to be in places other than RSS readers and browsers. Microsoft is focusing on three things in Vista around RSS : (Image courtesy : Michael Affronti) Category :RSS +Vista, Emerging Trends | Om Malik’s E-Book Of His Best Posts To celebrate the crossing of publishing 5000 posts, Om Malik, has created an e-book of the top 20 posts. Om Malik is an evergreen favourite and clearly an inspiring name in the blogosphere. I follow his postings quite regularly and am delighted to see the e-book presented as Christmas gift. Among the posts included in the e-book include ,Om Malik’s well known posts like Category :Blogs | Saturday, December 24, 2005The Digg Phenomenon & Its Robust Ecosystem We recently covered the phenomenon called digg. Digg started with the notion of how to leverage the collective mass of the Internet in various ways: applying it to content, using it to rank content, using it to make content more palatable to the masses. Automated systems take time to crawl the net. Editorial systems have the human factor. They may decide they're not interested that day, or they'll do it tomorrow. Category :Emerging Trends, Digg | Web 2.0 : Brickbats Galore But Hope Persists The Blogosphere is getting to see a lot more strong views on Web 2.0. Not withstanding the galloping progress seen, Richard McManus called Web 2.0 is dead and Russel Shaw wrote web2.0 doesnot exist. Dave Winer provides the best perspective. As he rightly sees it - there are two schools on "Web 2.0." Category :Web 2.0, Emerging Technologies, Emerging Opinions | Geoffrey Moore, Strategy ,Business Models, Long Tail & Optimization The latest issue of Harvard Business Review, has an article titled, Strategy and the Stronger Hand written by Geoffrey Moore, where he talks about two distinct models of businesses. As Geoffrey sees it, there are two kinds of businesses in the world – knowing what they are and which one your enterprise is – will guide you to the right strategic moves. In the complex systems model,enterprises can service large customers and can gor the customer base with large deals centered on mimimal number of transactions. 1000 customers provide a billion dollar business.In the other kind of business, the model is entered on volume operations – here the enterprise is on a hunting mode and strive to acquire millions of customers with significant number of transactions – Say FMCG enterprises. Category :Geoffrey Moore, Long Tail | Friday, December 23, 2005Gamechanging Blogs, Future, Maturity & Pulitzer PriceSramana Mitra writes, "with the advent of such phenomena as blogs and podcasting, a new era of democratic electronic media publishing has arrived". Excerpts with edits and comments added: Democratic new media publishing enabled at the click of a post-and-publish tab with relatively easy-to-use software wherein text, photo, and video blogs are the most popular forms.The nerds have suddenly set free the liberal arts types in droves. The phenomenon is well at work, and it will change the rules of the game for creative professionals world-wide. It will also change the rules for marketers and brand-builders. It expands the reach and ability to communicate with this universe exponentially, literally within minutes and help in monitoring trends and have other experts participate and contribute; the net effect being a richer and deeper knowledge base. With time, more people will take advantage of these democratic new media publishing opportunities. More serious writers and creative professionals will learn to market and sell their work using the Internet. Micro-payment mechanisms will mature, ad-supported business models will improve, and auctions of good work will become possible. A quality evaluation system will start to emerge as we go along. Good writers, good audio broadcasters, and good filmmakers will be able to monetize their work abundantly and creatively. She boldly goes ahead to predict that there will be the equivalent of the Pulitzer Prize for Internet content—equally prestigious, equally well respected, equally well-regarded. Quality content that's published, managed, distributed, and marketed through blogs, video-blogs, photo-blogs, and audio-casts, is a macro-phenomenonA well written note – and if I may add, with the dizzying growth of the blogsphere the distinction between the big, high-traffic blogs and the rest of the world of blogging will be increasingly sharply polarized. Somebody predicted the end of the individual blogger- though it has not yet happened in a pronounced way. There would come a day when we can see where top bloggers won’t be just viewed as mere bloggers but would be seen as doing something very different from the rest of the folks.. Category :Blogs | FT Names Google’s founders As Men of the Year Google’s founders may have conquered the internet world in 2005 – but given their outsized ambitions, this may only be a start. Sergey Brin and Larry Page are named as Men of the Year by the Financial Times, harbour hopes that reach well beyond their search engine business to “make the world a better place”. Image Courtesy : AFP/Google-HO/File Category :Awards, Google | FOSS Movement : Winning The Hearts & Minds Of The Indian Programmer Gervase Markham highlights that the US companies, being squeezed by low-cost, high-work-ethic competition from Asia, are looking to cut overheads by outsourcing their IT jobs – most of these go to India, as the country leverages the widespread knowledge of English, a legacy of its colonial past. In terms of the global IT landscape, it is perhaps more significant. As it is becoming uncontestedly clear that NPDI efforts shall be outsourced more aggressively in the coming months, there is also an invisible battle that is going in to win the battle for the hearts and minds of those tens of thousands of Indian software developers. Just as in the American market, on one side are the large commercial enterprises like Microsoft, hoping to tempt them with visions of a smoothly-integrated development system from a single vendor. On the other side is the free software movement, talking about the importance of liberty, unrestrictive licensing and control of your own computing environment. At stake is the ability to harness the brainpower of an entire subcontinent of hackers. During his recent trip to India, Bill Gates talked about recruiting top class Indian talent through innovative competition – this created huge publicity. By contrast, the FOSS.IN conference, a week beforehand in the very same venue, received comparatively little publicity. Microsoft & Opera Browser John Dvorak sees in Microsoft's announcement that it wouldn't upgrade the Internet Explorer for the Macintosh, leaving that market segment to apparently languish and gravitate towards the Safari browser and Firefox as to be watched carefully . Microsoft does not give up markets with a whimper. Something is brewing. The smart move for the company would be for Microsoft to discard the entire code base of Internet Explorer and buy the Opera browser (from Norway) outright and use it instead. Cooltechzone reports that an insider reported that both Microsoft and Google were trying to bid on Opera, but in the end, the software maker took the lead... Perhaps the most desirable feature that Opera has to offer is its mobile version of the browser. Thus far, it’s the best mobile browser currently on portable devices, and it will surely give Microsoft an easy entry into the mobile market, especially as that market continues to flourish gradually. John is right in his assessment that regaining momentum in the browser business is important to Microsoft since the browser has quietly become the mechanism of choice to lead people into search engines If this happening, the biggest loser might be Mozilla Firefox since many consider Opera to not only be the best browser available, but the fastest and the one with the best page rendering engine. AMR On Enteprise Software Trends In 2006AMR’s Bruce Richardson has a set of predictions for 2006 in the enterprise software industry.Predicting a strong year for the enterprise software and services market – he points to five major growth themes for the coming year. Category :Technology Predictions 2006, Emerging Trends | Wink Launches Search Engine That Combines Tag Results Courtesy of Techcrunch saw this annoucement of the launch of Wink. Category :Wink, Emerging Technologies | |

| Sadagopan's Weblog on Emerging Technologies, Trends,Thoughts, Ideas & Cyberworld |