Courtesy of Prashanth Rai came across this global outsourcing guide. The report starts by highlighting that India remains the leading offshoring destination by a wide margin and with every passing year, the risks of moving work to India are coming down. Usual noise – china’s role can get bigger, Eastern Europe may be found attractive by western European nations and Latin American nations will increase their share and African nations can follow suit so says the report. Not to ignore the fact that the Russia services source is growing fast. It’s a nice report, the facts presented in a structured way, looked good. What intrigued me was a naughty statement(if I may call so) attributed to Davidon of Nautilaus that India’s market share may go down from 80% to 10% in the next 4 years!! - clearly the statement can’t even be considered for inclusion in this guide which says is built on research findings from the likes of Gartner, Everest, A.T.Kearney, NeoIT etc. My take : Factors that influence the choice includes talent pool, cultural affinities, geographical proximities, cost structure and ability to scale etc. In general, what I find is that most of the commentators are a little soft on the emerging locations for offshoring – as I see it many of them do not attach the same importance when they write about key issues like attrition and scaling up. For example, people in the business know the alarming attrition and higher costs base when it comes to looking at China for offshoring, while I do certainly expect most of the emerging locations to increase the volumes, in reality I am not sure if any one country(other than china) can be the miniature equivalent to India – even on a scale of 1:XX in a sustained way. A recent assessment on china’s potential makes an interesting reading.

All these relate to IT Services outsourcing and when it comes to process outsourcing, practically every developing country starting from Tunisia to Brazil want to be a part of that It appears every consulting company in the world today is engaged in advising various government and government bodies on how to position & promote respective nations as an attractive destinations( one can therefore expect more location study results coming out - making a movement out of it!!). While government initiatives may not matter a lot in the long run, clearly the BPeS sector may see a better spread across nations. Over a period of time, the location preferences may matter only to service providers or useful for those planning /maintaining captive centers and customers may prefer to manage things through commercial negotations and service levels.

But there are larger issues at interplay : The focus now needs to shift to improving productivity & yield coonverting into better business value as can be seen by executing faster and providing better business solutions. As I wrote recently, sourcing relationships actually encompass a wide array of choices given the dynamic nature of business and the intersections of various levels of capabilities that lay within enterprises and service providers. The increasing expectations associated with outsourcing are becoming difficult to meet. With a wide range of functions getting outsourced, the ability of the outsourcer to bind and manage all these functions meets with a varying degree of disruption. On the other hand, the service providers are coming under huge pressure to improve operational efficiencies and to maintain and enhance margins. So in essence, seen from a customer perspective, offshoring strategies need to be dynamically re-evaluated as the business needs, strategies, models and execution methods keep changing. Clearly for the foreseeable future, despite the higher salaries experienced in India and other offshore markets, customers can continue to work with their chosen offshore service provider out of the existing locations to maintain the cost advantage besides reaping a set of other known higher-order benefits in offshore outsourcing opportunities.

In the microsoft analyst day presentations, Ray Ozzie summaries the trends that he sees today : The world is evolving into a highly networked form in which the barriers to participation in almost everything we do are crumbling down—the barriers to sharing, the barriers to contributing and learning, the barriers to working together. As more participants come online, platforms and marketplaces will serve to make exchanges more liquid and more efficient. He also identifies that there’s a fundamental transformation toward services and service-enabled software and Microsoft is investing to utilize services as a means to grow existing and new businesses. How’s Microsoft responding ? He says, The three most fundamental underpinnings of the approach are: - First, to continuously increase the number and quality of the service-connected offerings from desktop to Web, to naturally and organically attract users and increase usage. - A second key underpinning is to continuously increase the ability to optimize the offerings using the aggregated data that the platform infrastructure produces,in a secure manner. - And the third key factor is to significantly increase the seamlessness of the experiences that users enjoy across multiple PCs and other devices.

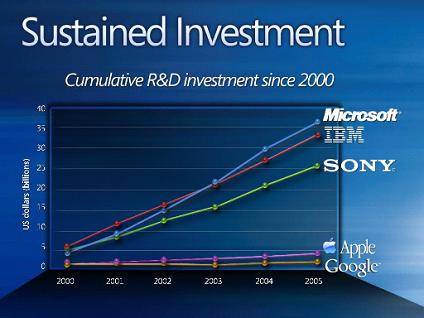

Craig Mundie’s presentation tabulates the reported R&D investments amongst the technology majors. Shocking to say the least when seen together. He points out that big changes take time and effort and highlights the type of innovation that Microsoft is after – on the disruptive, responsive and sustained spectrum. Microsoft spending details is not helping them win the respect of the tech watching community. Innovation on the products/services that most of what the world associates with Microsoft (centered on the desktop) is seen happening in the sustained category – precisely where many see Microsoft to be ineffective/slow moving and seen to be losing ground(MSN search?). Not that it has set the market on fire through disruptive innovation - if anything in the mobile/pervasive/CES space, it is seen that others are defining the agenda. While some cyclical investment surge is understandable – what we are seeing is a trend of progressive increase in spending . Paul Kedrosky points out that Google has added over a $100-billion in market capitalization during the period, while Microsoft has shed around $30-billion in market cap. Similarly, Apple has added around 30-billion in market cap, while IBM has shed around $20-billion. As I see it, after all, Apple is rated as the most innovative company by Fortune. As I wrote earlier, one does not necessarily need to spend about five billion in R&D to find that the next big thing does not exist. As Michael Scrage recently wrote brilliantly, the simple fact is that "R&D spending is an input, not a measure of efficiency, effectiveness or productivity. Ingenuity, invention and innovation are rarely functions of budgetary investment & points to the fact that Wal-Mart, Texco and Dell have miniscule R&D budgets, their quality, procurement and growth requirements have probably done more to drive productive innovation investment than any competing initiatives. Growing market competition, not growing R&D spending, is what drives innovation". A successful innovation policy is a competition policy where companies see innovation as a cost-effective investment to differentiate themselves profitably. It is not proper to confuse the number of patents as an index of innovative abilities. In general, process innovation is far more powerful than product innovation – it has a multiplier effect that product innovation can rarely match - the best way to look at innovation activity is the rates of productivity improvement in value add inside enterprises measured against the number of employees Its clearly organizational interest, result orientation, quality of leadership and the latitude the research team has and the integration that business and research has within the enterprise that matters a lot. Clearly these are the factors that get severely affected when organization grows. It’s time to look at assessment of new product /new revenue streams coming out of enterprises(Microsoft in this case) lot more closely as they begin to grow.

Days after my return from the US, I was on a brief trip to Beijing, China last few days and just returned back home. The city of Beijing was full of fog - almost dark throughout the day. Beijing is splurging – the development of Beijing continues to proceed at a rapid pace, cranes are booming everywhere in preparation for the 2008 olympics. I contrast that with the slow growth that I see in India. The IT industry is just beginning to grow there. As I met with a cross section of people – Global IT giants, business majors etc- I understood that, and the vast expansion of Beijing has created a multitude of problems for the city – home to some 16 million people. Frequent "power-saving" programs have been put in place by the government. Beijing residents and regular visitors often complain about the quality and cost of the basic utility services – water , electricity & natural gas. Efforts to control the smog include the government ordering industries to control pollution and leave the Beijing area in an effort to control the smog that covers the city. Morgan Stanley’s Andy Xie thinks that china’s environment catastrophe is poorly understood. He points out that if the relocated factries had to subscribe to the same environmental standards as in the OECD countries, goods made in china may not be that cheap and adds that the lesser costs for pollution have been important than cheap labour in the deflationary pressure from china. While it was frustrating to see that blog domains are blocked from within the country, I must say that the progress in Beijing(an old city in some ways and very different from the Chinese chow case city of Shanghai) is indeed amazing. Not to forgot the shopping that one can do in the backyard of the world's factory.

That’ why it is interesting to see what china watchers have to say about the progress made by the nation.Jim Jubak writes that the imminent downturn in china could hurt global economy significantly. As he sees it, post the Olympics boom, The Beijing government has prepared for a rise in bad loans as a result of an economic downturn by selling off stakes in the country's biggest banks to overseas investors. The government has guaranteed that some of the world's deepest financial pockets will be available to bail out China's banks in the next crisis. He adds that china produces an impressive 600,000 university-trained engineers annually. But thanks to an educational system that stresses rote and memorization, McKinsey calculates that only about one-third of those engineers have the skill level demanded of an engineer by a global economy. An underemployed and dissatisfied class of university graduates is far more of a threat to the government of a developing country than unrest among the peasants.Read his article here. As I see it, besides influencing the global economy in a significant way, the truth is that millions and millions of people have gotten to lead a better life and more and more are becoming prosperous.

The supposed talent shortage in India is again making the rounds. The Tier 1 Indian offshore majors – TCS, Infosys, Wipro & Satyam all have exceeded guidance for the first quarter and have revised their guidance upward for the financial year. All the four majors are working almost at near peak loading, as reported by them. The results of cognizant are expected to be declared next week and almost analysts expect them to report good numbers. The Tier 1 Indian headquartered firms continue to make huge strides and despite some attendant difficulties in scaling up(which they are addressing quite well) they are seen to be executing very well, restrategising and as needed realigning their approach - seen from an operational, financial, competitive value add, efficiency perspectives. The surging confidence is palpable. As I wrote recently, on all conventional financial metrics – Growth, margins, offshore firms have established new records. Average attrition levels at offshore firms are far less than that reported by the likes of Accenture – across quarters – an important trend to watch. Talk of some having mastered the global delivery model gets decimated by the fact the average billing rates for firms in the commercial firms stand approximately three- four times more than that of the offshore firms. The expanding opportunity for offshore services is indeed real for all to see. A model built to study this interplay and to evaluate various scenarios for different industries shows that approximately 35 percent of the work that could potentially be offshored, worth $110 billion and divided equally between IT services and business processes, actually will be offshored by 2010. Mckinsey believes that India's offshoring industry, which has captured two-thirds of the current global market for offshored IT services and almost half of the global market for offshored business processes is poised to grow faster, The spotty area is of course means to correlate productivity increase. Industry captains exude confidence about the Indian education system with some rejig can help in the supply situation and help maintain the leadership position. The sustainable advantage and favorable drivers are indeed proving to be real and gaining strength.

Lee Gomes brings out in WSJ his arguments as to why the Long Tail phenomenon is not significant. As he finds the phenomenon presupposes that while traditional companies are limited by shelf space to offering only a relatively small number of "hits," on the Web, they can carry a vastly bigger number of slower-selling items. These "misses," which make up the "tail" of the title, can, he says, add up to a big number - maybe even bigger than sales of the hits.By Mr. Anderson's calculation, 25% of Amazon's sales are from its tail, as they involve books you can't find at a traditional retailer. But using another analysis of those numbers - an analysis that Mr. Anderson argues isn't meaningful - you can show that 2.7% of Amazon's titles produce a whopping 75% of its revenues and he sees this as not quite as impressive.

Anderson responds with a lot of reasoning and highlights that trying to define "head" and "tail" in percentage terms is meaningless in a market with unlimited inventory, because the denominator can grow infinitely large. Giving an example, he says that with 1,000 items and the top 100 (10%) account for 50% of the sales. Then you add another 99,000 items to the catalog, and the sales of that top 100 fall to just 25% of the total, while it takes another 900 items to make up the next 25%. Here the demand has shifted down the tail, because those top 100 items have dropped from half the market to just a quarter of it and the rest of the demand is spread over more items. But by Gomes' math, we've gone from a market where 10% of products make 50% of the revenues to one where 1% of the products make 50% of the revenues--in other words, it's become more hit-centric & he thinks(not without reason) this is simply a misunderstanding of basic statistics.

As I see it it is obvious that the internet has brought out the long tail effect – the differences stem on account of two things : is this growing (Anderson says yes, Gomes says No), is it all that significant (opinion is mixed here – we have to see which business entity is largely successful owing to the long tail . A recent Slate magazine article seems to suggest that it is more mixed – for now atleast for online magazines. – even the poster child of the long tail phenomenon –amazon.com is as seen by some - testing investor’s patience (though business success may depend on many other factors). In fact Amazon finds that the rush of companies online has made it harder for it to maintain customer loyalty or offer the best deal, as people grow accustomed to browsing the Internet for the lowest price (in a way this hypethesis questions the validity and usefulness of the long tail). Just as the oft repeated statement in the long term things would work out for Amazon, it appears even the long tail phenomenon may help business in the long run. The long tail phenomenon needs to have consistently outperforming business as its reference, till then it would appear to be not so clear to observers as to how large and long is long (both the tail and the time).

Mercury which made an acquisition recently – one that of systinet is now in the process of getting acquired by HP. May be they wanted to spruce up their stodgy image.(I expected that HP may make a big ticket offshore service player acquisition, given their relatively poor scaleup in low cost countries and HP services not making any big moves in the recent past). Sungard makes a bid for System Access. The first move is an infrastructure play and the second one brings together vertical solutions. On paper, appears good - though for HP, acquiring Mercury is a real big move.

Jeff Nolanwrites that in a scenario where, customers are already conditioned to expect a huge discount on the list price for the software, so going to zero, or close to it, synchronizes the actual price list to the official one may be more sensible. He points out two important things: - License sales are simply a proxy for the future annuity that a maintenance base is. If the core application functionality that is competitive neutral as free, large installed bases can be built & consequently the complete sales cycle mechanism would change. - Enterprise software selling favors the large vendors at the expense of the rest of the market & the sales processes don’t facilitate selling across the entire market spectrum and that’s where he sees partner’s fit in. ( I see a much bigger role for partners – from recommendations to making the value proposition real, they play a much more important role seen from a customer perspective – in fact when software gets commoditized, the differentiation and scope for value add remains entirely on services. Also the services revenue of the product vendors are not small money as reported).) He argues that the cost of sales can be lowered while horizontally scaling the customer base & the objective of the sales could be the upselling of components and maximum penetration of existing accounts. Sales become monetizing the support part of the deal and moves away from the promise of upgrades. As he sees it the risk for product vendors here - newrange of competitors that could price cannibalize the entire business and that this approach could be in essence cannibalizing billions of license revenue for the prospect of rewards in the lower margin services business. Other obstacles include compensating sales team and reporting financial results. Challenges would include devising new rules for support pricing models, offering the “Core” software free and charging for the context – vertical solutions, technology add-ons like analytics components etc. My Take : These are all sensible ideas, no doubt. Jeff ought to be complimented for thinking out of the box here. I think that the customers would benefit here only when true interoperability becomes possible, composites becoming more rampant and the ability of the vendor/vendor consortium to help and support customers in such scenario becomes crucial. The Obstacles look substantial – they could overrun any chances of such innovations/changes happening!! Megavendors should not make it look like they are creating a new operational model, when the traditional license growth for conventional product sales are seen to be showing limited growth. As I see it there are improvements that need to happen on multiple fronts for the existing customers and are more overwhelming. In general, it can be easily seen that all aspects of software spanning technology and markets to usage and licensing models, will undergo substantial change in the coming years. Vendor consolidation & instance consolidation are making things more and more tough for customers with the switching costs making exit almost a non existent option. Product vendors benefit when organizations over-customize their systems or become extremely reliant on the vendor without having thought through and bringing in contractual safeguards. Vendors need to dicuss and provide options for the different types of license audits that they can choose to make – the threat impact and the risk mitigation costs for the customer here are really huge. Vinnie points to a computerworld investigation involving 51 companies - including 14 that Microsoft contacted about the SAM program - showed that many U.S.-based IT managers were confused, distrustful or downright angry after their companies had been accused of potential licensing problems Some of the recommended protective measures include - protecting license costs for additional users and a provision to account for unused software or user base ought to be built in. Software companies ironically try to make money when users switch the hardware platform! – it is imperative that buyers make provisions during negotiations in contract to build in the ability to transfer rights in mergers and acquisitions or hardware updates. Buyers should be able to upgrade hardware / change site locations without the burden of additional costs. The whole notion of a perpetual license is that buyers own it and use it as they deem fit and the machine and location should simply not matter, except in legal restraints imposed by different nations. Customers ought to have the rights to exchange the license in case of version switches with same functionality for no additional license, maintenance, or support cost. Just as charity begins at home, changes ought to start from the current base - though it may be a tall order to expect mega vendors to change their ways overnight, particularly when the going looks better for them.

I wrote a brief note on Enterprise Software & The Future Of Smaller Players. I began writing this note as I arrived in the Valley for a brief visit and concluded the note as I was about to fly out. I passed through several buildings which hosted a number of enterprise software players, I met up with some of them as well - while I work with a number of them across the various continents. As I see it, there is a crying need now for a new structure for the enterprise software ecosystem wherein the smaller members can participate and benefit in a fair manner from the opportunities that are arising in this space. Brutal waves of consolidation, investor reluctance to fund enterprise software startups, the not so firmed up patterns on corporate buying of enterprise software – all have gone to directly affect the prospects of a number of small software companies. The distinctive factors between the aspirants, contenders and pretenders of the enterprise software industry trying to work in this segment are quite interesting to watch. The landscape of the enterprise solutions is still dotted by the all–rolled–in-one type of solution players to niche focused players with well defined solutions. The irony is that such players are running the risk of being marginalized – not just by the natural law of economic forces alone – but by the inelegant, self hurting greedy designs of the mega vendors/their stakeholders. While the top-tier vendors boast of wide ranging integrated functionalities with deep pockets, specialized solutions like PLM, SRM, MDM, Content management, BPM, Document management, Compliance solutions, Vertical solutions coming from best - of - breed players continue to remain attractive to buyers of different spectrum. The mega vendors are trying to counter this competition with promises of rapid deployment methods and attractive packages of fixed time, fixed price based accelerated rollouts with templatised approaches. Again for reasons centered around concerns of integration and cohesion, even these options are proving to be seen less attractive by prospective buyers. Prefabricated/Cookie-cutter/fixed term/price – all look attractive on paper, in real sense these do not satisfy the prospects, despite these being medium/small business. This forces onerous responsibility on the mega vendors to offer solutions that are not only cost effective, less complex and faster to implement but offer open solutions that can be extended over time and be amenable for efficient version and technology upgrades

Owing to continual pressures of consolidation, newer trends are emerging: the trend that these consolidation are effecting more than reducing the number of players in the enterprise applications field, it is contributing to the widening the gap between application/infrastructure mega vendors and pure-play application providers. What can this lead to : This way, in the medium to long term, the leadership status that the mega vendors want to hold on to may slip away – faster than it took for them to build. After all being in touch with the application ecosystem, matching customer expectations are a basic requisite for enduring success and fostering innovations. Clearly, the enterprise software market will have to reflect and embark on an important restructuring and transformation to become more vibrant, broad based, innovative and bounce back as a serious contributor to the growth of the industry ecosystem and the business at large. Read the full note here.

I always enjoy reading Nandan Nilekani’s views – he is clearly one of the most articulate CEO's in the global IT industry today ( not necessarily just the indian headquartered companies) and am amazed hearing him/reading him when he responds to issues on the fly with so much conviction, depth and choice of words. In the recent Q1 analyst call he was on the feet in his response to rising wages and how this might not be a competitive disadvantage to Infosys, He said in response to a query that it’s important to understand that what is happening here with systematic values of Infosys are coming up on different facets of our business. 1. First of all, I think the size, brand and scale is building one barrier of entry. 2. The $100 million a year investment in training is creating another barrier of entry. 3. The compensation package is creating a barrier of entry. 4. The growth rate is creating a barrier of entry, because what happens when you have high growth rate is that you’re able to essentially spread the cost of competition over a pyramid. When a company’s growth rate goes down, then it ends up becoming top-heavy and it reflects in its per capita employee cost. He further argues that organizations need to have a high growth rate to pay for all these things. Essentially, we are trying to create a virtual cycle which we believe will lead to further consolidation from the pack. Powerful statements - quite insightful.

I read in my return flight to Singapore, the Financial Times interview with Nandan Nilekani. Jo Johnson writes that Nandan Nilekani makes clear that India’s business success is payback for centuries of economic exploitation. "The juxtaposition of India and China is a consequence of what we’ve achieved on the services side," he says. If India is creating job insecurity in OECD economies, he certainly feels no need to apologise. "I don’t think that a high standard of living is an entitlement," he says….. "I don’t think the world can live with everyone driving an SUV. Something’s got to give. It’s just become more competitive. If Indians and Chinese can work 80- 100 hours a week and they are part of a global, fungible labour market, it’s going to have an impact on living standards in the west."….."I believe that the tide has turned," he continues. "Two hundred years back, India and China were 50 per cent of global GDP, but both, for different reasons, opted out of the race. In China, they turned inwards and in India we had the empire. The next century is an opportunity to redeem some of that: the flat world has created a unique confluence of circumstances which will have a huge impact on all our lives." Without getting offended - read his interview along with this businessweek cover story talking about a wider theme.

I also liked Nandan’s definition of Ideas Entrepreneur – while referring to Tom Friedman. He says, Tom Friedman is an ideas entrepreneur” and adds. "Entrepreneurship in business is about a guy who has the best idea and acts quickly to get his product to market. He's the intellectual equivalent." No need to worry guys in the US - offshoring is today an industry still in its infancy, with more than 90 per cent of the addressable market yet to be tapped and the US market is quite vibrant and flush with opportunities. After all US companies involved in offshoring are seen to be witnessing extraordinary productivity with the available resources. As David Kirkpatrick wrote sometime back, more than 90% of the world’s population growth through 2050 is projected to take place in poor countries & the US is just 290 million in a world of 6.4 billion people. Opponents of offshoring idea need to start thinking harder about what that means.

In this week’s cover story, Emerging Giants, Business Week explores the phenomenon of multinationals emerging form the developing nations competing with the traditional western multinationals. The article says,"A new breed of ambitious multinational is rising on the world scene, presenting both challenges and opportunities for established global players.These new contenders hail from seemingly unlikely places, developing nations such as Brazil, China, India, Russia, and even Egypt and South Africa. They are shaking up entire industries, from farm equipment and refrigerators to aircraft and telecom services, and changing the rules of global competition". John Seely Brown and John Hagel suggests that if western enterprises are not participating in the mass-market segment of emerging economies, they are not developing the capabilities needed to compete back home. They called it innovation blowback - referring to the phenomenon that businesses from the developing world that expand into overseas markets and go head-to-head with established multi-national corporations. The duo had been recommending that by targeting the specific and demanding needs of lower-income consumers, Western companies can address a far bigger emerging-market opportunity and create the ability to take innovative products and services from the emerging world and use them in new categories at home.

C.K.Prahalad had been repeatedly talking about the different nature of innovation happening in the emerging economies. Look at what happens when good corporations first begin to work in the more challenging emerging economies : they get seasoned enough to become to be more adaptable and, consequently, more fit and ready to thrive in the hyper competitive global marketplace. "Hardscrabble origins", as Business Week writes, "can be a vital source of strength. These companies have learned to make money by developing reliable, easy-to-use goods and services at very low prices." To get an idea of the distribution of such enterprises – look at the fortune list of Top cities where Global 500 corporations are headquartered. Many people make snide remarks about asian headquartered companies making more margins than western corporations – the article provides the reason –"Unlike Japanese and Korean conglomerates, which benefited from protection and big profits at home before they took on the world, these are mostly companies that have prevailed in brutally competitive domestic markets, where local companies have to duke it out with homegrown rivals and Western multinationals every day. As a result, these emerging champions must make profits at price levels unheard of in the U.S. or Europe". Without any more words, I recommend reading the full article here.

In my flight out of San Francisco, read the Pew Internet titled Bloggers: A Portrait of the internet’s New Storytellers. ( Am posting this from Incheon Airport,Seoul during the less than two hour stopover enroute to Singapore). The report looks good and most part of the report findings I concur with. It is important that the blogosphere and the society at large understand the blog movement – examine it form multiple perspectives, collect various perspectives , look at ways and means of building this movement –examine the value of the social network community that gets formed. At least it can keep at bay irrational attacks like the one that Forbes recently made on blogs.

Some of the key findings of the report is summarized as:

- Blogging is bringing new voices to the online world. - Just 11% of bloggers say they focus mainly on government or politics. - The blogging population is young, evenly split between women and men, and racially diverse. - Relatively small groups of bloggers view blogging as a public endeavor. - The main reasons for keeping a blog are creative expression and sharing personal experiences. - Only one-third of bloggers see blogging as a form of journalism. Yet many check facts and cite original sources. - Bloggers are avid consumers and creators of online content. They are also heavy users of the internet in general. - Bloggers often utilize community and readership-enhancing features available on their blogs.

In my quick scan of the report,I could not find how top executives, CEO’s and industry analysts don the role of bloggers – a point that I had brought out earlier or on the massive impact bloggers are making in some arena. (Image courtesy :Pew Internet report) Category :Bloggers, Emerging Trends

Recently Bob Cringley felt that IBM was on the verge of a disaster – pointing to lack of innovation and claimed it is surviving on customer inertia and clever advertising. A recently released UBS report on IBM says that due to company-specific execution issues, IBM isn't the proxy it used to be for the services space, especially in consulting/systems integration. Key points include:

- Some company-specific services softness in IBM's 2Q services results are reflective in part of co-specific issues (i.e. PwC integration & turnover) rather than industry-wide demand conditions. - Outsourcing signings down significantly LT signings of $4.6B declined 50% y/y & 12% on a TTM y/y basis (tough y/y comp & notably longer sales cycle).

A computerwire report that I came across captures the point the new bookings are showing a declining trend. The figure(courtesy of computerwire) captures it all: I do not want to say anything on the above – but in general, come to think of it - substitute IBM with any other known name from consulting & services industry – would it look any different –unlikely barring a few.(I do know of a few really having different models, metrics and approach). The whole service industry and enterprise software industry plays on the customer inertia and lack of an alternative. Whats that disruptive model that would shake up the services industry – clearly offshoring played that role to an extent but the laggards seem to be catching up here/atleast make up an appearance of catching up. Seen from a service industry perspective, next technology breakthrough heralding new opportunity could help them rejig their model – like what BPR/ERP wave did earlier or the dot com era – SOA is still many years down the line. Seen from a customer perspective, how does one lock themselves out of this ? Seen from an investor perspective, how to value service companies where increasingly the differentiation factors seem to be just the scale and historical presence.These are definitely key concerns. Innovation inside consulting and service organization needs a different mindset to foster and manage - clerical approach shall have deleterious effects.

I had been covering about the limitations about the chinese service players and the market and why china may not be a significant force in global consulting & services segment. Gartner’s Rolf Jester writes after attending the second china international software and information service outsourcing summit (CSIO) in Dalian, on china’s potential to operate in a major way in outsourcing services market and he thinks that chinese providers have a long way to go for being called a success in the global services arena. Highlighting the lopsidedness in the industry’s thrust in china, he says, providers should focus on reaching potential overseas customers and spend less time on internal conferences. He is on the dot when he observes that wWhile most of the firms are just focusing on cost savings, the hard reality is that enterprises need develop their own unique value proposition beyond cost saving to service it for the long term in the global market. Cost advantage is sustainable only till the extent of time even-less-expensive country gets "discovered" by buyers. The overwhelming majority of IT services companies in China have a long way to go to become successful exporters of services to the wider global market. Chinese firms predominantly serving customers in Japan are doing ok and are mostly working on embedded software for high-tech vendors – a high proportion of IT services exported from China is accounted for by testing, localization and maintenance of products, especially embedded software for high-tech vendors in Japan and the U.S. There are also quite a few captive offshore centers in China that are owned and managed by high-tech companies from other countries, including the U.S., Japan and India, doing product development and maintenance . The Chinese government statistics show, 65 percent of Chinese IT services exports go to Japan. Japanese complain about communication issues and there is fierce price competition in the Japanese market for the lower-value phases of application development, such as simple coding and unit testing. The main target customers, Japanese systems integration (SI) firms, are facing lower profitability themselves, thus putting additional price pressure on their Chinese suppliers. The possibility of an appreciating chinese currency exacerbates that risk. At best, other global vendors including offshore majors can consider chinese services firms as suppliers of services, as part of a value chain or as potential acquisition targets. Most Chinese companies do need a large global partner to help them adequately address the global market. There is a real case for assessing predictions that most of the Chinese providers would wind up their export business in the next 3 or 4years as a massive consolidation/re-alignment happens in the industry.

It is with a certain tinge of amusement & sadness that I read about the exit of top brass of Sify. The rumoured exit of top leadership is quite unlike what we see in Indian headquartered companies. I know most of the sify top team quite well– and am watching sify at close quarters for almost a decade. I have seen sify bloom from a whiteboard idea to what it is today. A path breaking company, it underwent major changes and was beginning to look attractive. Sify always brought out mixed out emotions from observers – but everyone I speak to accept that Sify is sitting on a goldmine with its I-Way cybercafé spread across all over India and it had been far ahead of its time since its inception. I do not know of one listed company in Asia which could go after so many acquisitions in so few years time and could be more daring than Sify. I recently heard about their plans to expand into other geographies and focus on managed services in the US. Turnover at Sify was always very high – many in the corporate world in India would have some connections with Sify and in a true sense, it also managed to attract many senior executives from traditional industries to join the internet phenomenon that it spearheaded in the country. Sify.com is perhaps one of the richest portals with so many channels built inside in India - their corporate networks division was their biggest and the portals were easily the most underleveraged. Sify is an Indian internet world Icon – a pioneer of sorts on many things in India and certainly has a glorious future ahead, its recent performance is a testament to this. Let me stop at this - I know so many things about Sify and people associated with Sify -it may not be proper for me to elaborate further but would like to say that the top honchos of Sify would be found great picks by others in the industry.

Nick Carr is right in his observation that the disparaging reaction to Dell's effort shows that establishing a corporate blog is not a risk-free proposition.I earlier covered the Fortune 500 blogging phenomenon. The Fortune 500 Biz blog list or the expanded global 1000_business_blogging Global 1000 list makes interesting reading. The crux of the matter is that some see that the risks and uncertainties of public business blogging are so great that big companies only do it under duress, when their traditional corporate messaging has lost traction. So companies on the way up don't want to mess with their success by introducing a new lens on the enterprise that isn't controlled by the PR department. Blogs become an automatic choice under such circumstances. The latest entrant is into the blogosphere is Dell and bingo, criticisms have already started surfacing about the blog. Dell's policy is said to be one centered on pre - approving posting and moderating blog comments. Sensible, as I see it given the fact that millions of customers use Dell products - The policy it appears is,in short, to approve anything that's on-topic, delete the stuff that's meant for sensationalizing things,direct specific issues to customer service and keep it outside the blog. The sanctity of the blog is that it is not just a redressal mechanism benefiting a few while millions can potentially read those!! While there may be criticisms about Dell blogs not meeting the exacting/expanding standards of classical bloggers, reality is that in life everything in life including blogs needs to have an objective and should be run on a certain defined method to succeed. Nick's rules of thumb viz. do not blog for the sake of blogging, there is no one right way for blogging, the blogs need to reflect the company's desired image and supports its strategy (let me add to the extent possible - but no doubt it is better to be atleast aligned). While, it may be true that the equity a corporate blogger builds up is portable, in other words. Rather than sticking to the company, it will follow the blogger -even if the blogger heads to a competitor. This is true of all professionals in the media, hospitality – nay most of the well known faces in the service industry. After all the standard of blogs can also improve over a period of time. Blogging is also a work-in-progress, so to say and finding a winning style adherent to commonly accepted norms happens over a period of time and sometimes could depend on the strength of the personality of the blogger and would only over a period of time gain identity and establish a meaning for itself –till then we have to wait and keep welcoming such initiatives and not be overly critical.

It appears that blogspot.com blogs hosted on Blogger.com have been blocked by some ISPs in India. Mridula has some related details. Apparently, one of the several ISP’s operating in the country confirmed the blockage. Connections through some ISP’s(most of them are big ISP’s) showed that things were normal. In effect within the country, blogs don’t really matter that much. The blogosphere hasn’t matured enough to have any real impact on Indian polity. Speculation is that maybe the government just wanted to block a few 'blogspot' sites and in the process the entire domain got blocked. I very much doubt that the Govenrment of India would do this deliberately or with the knowledge that the entire domain is blocked. But whatever be the intent the thought of filtering sites by blocking domains is simply not acceptable. India can not be in the infamous company of china and saudi arabia in blocking sites. I could not also avoid noticing the blogosphere coming up with ways and means to circumvent the blockage and still read the banned sites. Hopefully this is just an intent on filtering few sites that were wrongly taken by some small ISP’s to cover the entire domain – but if that is not the case – its stupidity –and would signal to dark age.

David Kirkpatrick has an analysis of Rocketboom that spent zero dollars in marketing and advertising,relying instead on word-of-mouth publicity was able to get 300,000 viewers for its vlog. Naturally this leads to questions about business model, revenue streams etc. David while highlighting that it has carried so few advertisements that it has probably made about $0 in profit thinks that Rocketboom is probably a strong indication of thigs to come in the user-generated media space. David writes:"In the saga of Rocketboom can be seen the future of media…But part of the reason the Rocketboom ruckus is so delicious is that the site has always devoted much of its coverage to the very phenomenon it exemplifies - the rise of consumer-created media. In fact, everything about Rocketboom is very right now…Little noted in all the coverage however is how innovative Rocketboom has been. It’s some of the best video you’ll see anywhere - as much video art as news. The audio is fantastic, the writing consistently sharp, and the subject matter surprisingly diverse and entertaining." You can read the full article here: The Rocketboom Ruckus here. As I see it, While the bullishness is based on user generated content and it associated premium value, I am not too enthused about user generated content itself given the proliferation of electronic media and rendering devices. If Rocketboom were to work on creating heppy quality content, then they are in an head-on collision with the traditional media – far more resourceful and showing signs of great dynamism and it they are just going to rely on user generated content, once can’t escape the fact that reality will dawn upon them as is happening with the likes of youtube. The hyped up Skype’s, Flickr’s provide ample lessons. A look at the way the posterboy of internet era - Amazon & its stock movement tells it all.

By seeming to assure that the value of a network would increase quadratically—proportionately to the square of the number of its participants—while costs would, at most, grow linearly, Metcalfe's Law gave an air of credibility to the mad rush for growth and the neglect of profitability. It was hot stuff during the Internet bubble. Remarkably enough, though the quaint nostrums of the dot-com era are gone, Metcalfe's Law remains, adding a touch of scientific respectability to a new wave of investment that is being contemplated, the Bubble 2.0, which appears to be inspired by the success of Google. Courtesy of Paul Kedrosky saw this article. The article points out, if a network of 100 000 members that we know brings in $1 million. So if the network doubles its membership to 200 000, Metcalfe's Law says its value grows by (200 0002/100 0002) times, quadrupling to $4 million, whereas the n log(n) law says its value grows by 200 000 log(200 000)/100 000 log(100 000) times to only $2.1 million. In both cases, the network's growth in value more than doubles, still outpacing the growth in members, but the one is a much more modest growth than the other. Much of the difference between the artificial values of the dot-com era and the genuine value created by the Internet can be explained by the difference between the Metcalfe-fueled optimism of n 2 and the more sober reality of n log(n).Incidentally, this mathematics indicates why online stores are the only place to shop if your tastes in books, music, and movies are esoteric. Let's say an online music store like Rhapsody or iTunes carries 735 000 titles, while a traditional brick-and-mortar store will carry 10 000 to 20 000. The law of long tails says that two-thirds of the online store's revenue will come from just the titles that its physical rival carries. In other words, a very respectable chunk of revenue—a third—will come from the 720 000 or so titles that hardly anyone ever buys. And, unlike the cost to a brick-and-mortar store, the cost to an online store of holding all that inventory is minimal. So it makes good sense for them to stock all those incredibly slow-selling titles. This difference will be critical as network investors and managers plan better for growth. The fundamental flaw underlying both Metcalfe's and Reed's laws is in the assignment of equal value to all connections or all groups. At some point, adding one person would theoretically increase the network value by an amount equal to the whole world economy, and adding a few more people would make us all immeasurably rich. Clearly, this hasn't happened and is not likely to happen.

The Brown & Wilson Group's survey of the "Top 50 Best Managed Outsourcing Vendors" is just released. Based on an extensive survey(one amongst the largest of its kind),it appears to have focused on demonstrably consistent strength in four survey areas: - Human capital performance - CEO commitment - Corporate direction - Leadership impact The list is available here. Its interesting to see therein, ACS was the only big six service provider to leap upward to command the top spot in the "Best Managed" ranking in 2006. Also look at the hotshot offshore vendors listed therein. Satyam has been ranked the world’s second best outsourcing vendor and the No.1 amongst Indian vendors - the list includes other well known names like Cognizant,Infosys etc.. The outsourcing "big six" are seeing their dominance challenged in the outsourcing deals that are in the TPI pipeline and in development. Over 50% of the of the $100 billion worth of outsourcing contracts due for renewal globally in the next two years - out of which $17 billion could come in the next six months - have a significant offshoring component "much of which could come India's way." The other challenge for the Big Six is the trend towards a larger number of smaller deals that provide entry for the growing number of global players looking for opportunities. With more client firms splitting up their contracts among several vendors, the average size of deals are coming down and the deals are being spread over a number of players including smaller players. Movement is to a bigger quantity of lesser, single-function agreements. Escalating use of multiple vendors is creating business prospects for an extensive set of providers, while mitigating the competitive advantage of the big six. That’s precisely where survey results like this and perspectives like thiscould help.

As I finish my week long travel and reached Singapore saturday night – I last stopped at Phuket,Thailand. During the three days while I was at Phuket for official meetings, I could also see that the city has recovered splendidly post Tsunami. Some new construction activities are also taking place. The Tsunami that spread across the Andaman Sea, The Indian Ocean & The Bay Of Bengal created mammoth damage and fortunately did not affect outsourcing in any manner. A friend asked my views on how I see the impact of recentbombay events

While I may not be so enthused to say this : the cold reality is that wherever there is economic prosperity and activity – terrorism and associated events are a fact of life. The hemisphere and continent does not matter here. The only thing that looks controllable under such circumstances here : the preparedness to respond back with minimal disruption to telecom networks( with in built redundancy) and the resilience of the society to bounce back. On both counts Indian cities score very high – just as New York & London showed to the world that terrorists can't disrupt business for more than a few hours.

Courtesy of Vinnie saw this note on the long tail of the services industry. A Gartner survey finds that the top 6 services companies (Accenture, CSC, EDS, Fijutsu, HP and IBM) combined have only - 21% - market share and a long tail follows. This makes interesting reading given that the big six are seen to be increasingly on shaky grounds. Ofcourse, Accenture keeps reporting good numbers in recent quarters. Close to Bob Cringley’s insightful assessment of state of things inside IBM, comes the news that IBM has begun shifting executives from its traditional computing business into senior positions in its giant services arm in an effort to inject new momentum into the flagging division. These days, IBMers talk about “productising” services, turning them into clearly defined offerings that can be marketed and delivered in much the same way that new mainframe computers are. Its small and medium-sized business unit, for example, now distributes a catalogue outlining its main services. The emphasis on applying product-style marketing and brand management to services has drawn hardware executives into some key marketing roles in the global technology services unit. Company executives described the unusual injection of hardware talent as an attempt to bring traditional product disciplines to bear on the services business. IBM aims to make services more consistent and “repeatable” by designing standardised processes that could be delivered in a uniform way around the world. Traditional product management disciplines have also been used to identify new markets and to design and market services to take advantage of these opportunities. The shift in focus represented a move to turn services into a global operation to match IBM’s other product-based units. Turning services, which by definition are delivered by people, into repeatable processes where IBM can get economies of scale, amounts to an organisational and cultural overhaul of significant scale. Its not only for IBM – The other big name – HP is struggling in its service business. It finds that big deals are hard to manage and that digesting a large number of deals can hurt earnings and that aggressive top-line growth happens at the expense of profitability. HP now believes that focusing on the smaller deals could be a winning strategy. As I see it the services landscsape is indeed becoming ripe for a major change. Come to think of it - substitute IBM with any other known name from consulting & services industry – would it look any different –unlikely barring a few.(I do know of a few really having different models, metrics and approach). The whole service industry and enterprise software industry plays on the customer inertia and lack of an alternative. Whats that disruptive model that would shake up the services industry – clearly offshoring played that role to an extent but the laggards seem to be catching up here/atleast make up an appearance of catching up. Seen from a service industry perspective, next technology breakthrough heralding new opportunity could help them rejig their model – like what BPR/ERP wave did earlier or the dot com era – SOA is still many years down the line. Seen from a customer perspective, how does one lock themselves out of this ? Seen from an investor perspective, how to value service companies where increasingly the differentiation factors seem to be just the scale and historical presence.These are definitely key concerns. Innovation inside consulting and service organization needs a different mindset to foster and manage - clerical approach shall have deleterious effects.

I earlier covered the BCG report of the top performers of the RDE 100 – that’s "rapidly developing economy." Of these, 70 are from Asia (China has 44, India 21) and 18 from Latin America.These are really big corproations - look at the impressive numbers :RDE 100 companies’ portfolios contain $520 billion in fixed assets, and, in 2004, they employed 4.6 million people with a payroll of $20 billion – purchasing $200 billion a year in raw materials and energy, $50 billion in parts and components and $40 billion in services. Typically these companies adopts these six models to make it to the top.

- Model one: Taking RDE brands global

- Model two: Turning RDE engineering into global innovation

- Model three: Assuming global category leadership

- Model four: Monetising RDE natural resources globally

- Model five: Rolling out new business models to multiple markets

- Model six: Acquiring natural resources

Companies from the rapidly developing economies may broadly fit into one of the six strategies. But there is a rider: while these strategies are distinct in principle, they often overlap in practice. The RDE 100 also have some features in common. First, all of they build on positions of low cost — a key competitive advantage of rapidly developing economies. Virtually all the companies are adept at learning and adapting. This is what enables them to learn the lessons of established companies. Moving forward, that might be their biggest strength.

Who amongst the RDE’s are doing well - Lets look at the data: The RDE 100 companies grew at 24 per cent year-on-year from 2000-04 while the India 21 grew even faster — 30 per cent. The RDE companies also earned operating margins of 20 per cent over sales, compared to 16 per cent for US S&P 500 companies and 10 per cent for Japan’s Nikkei companies. The India 21 beat the crowd again with operating margins of 25 per cent.

One classic case looks impressive : Mahindra & Mahindra , the Indian headquartered automobile major. So how does M&M venture into foreign markets? "We are trying not only to leverage cost, but we are also trying to give value and build a brand. Doing it alone requires more financial investment, but we are using more than one model," says Parthasarathy. For instance, in the bigger markets like the US, M&M rides alone. In smaller markets like Sri Lanka or Serbia it uses distributors. In China, which requires a far greater local knowledge in terms of the market and the legal framework, M&M has a joint venture where it holds 80 per cent. For utility vehicles and pick-ups, the company has entered South Africa. The company also has a fool-proof checklist for global forays. This ranges from guidelines on prioritising global markets according to the size and attractiveness of market opportunities, to the micro issues of taking the brand abroad. Generally speaking brands from unknown entities learn faster and are quick on the uptake – so long as their bearings and alignments are right, they tend to do better than peers – that may include well established global majors.

I am not so unduly optimistic about the Web 2.0 movement – I had been calling for a realitycheck for some time. But the enthusiasm shown in building this movement is indeed amazing and some of applications show promise of success.

There are some interesting new trends on the Web, and it's the nature of a phrase like Web 2.0 that adheres to them, says Paul Graham. He finds that a lot is different now from 1998. Web sites look different. Startups operate differently. People use the Web in different ways. The changes were gradual, but if you have a gradual change of sufficient magnitude, it starts to become a different world. He sees that technology is an ever larger component of business, so power is shifting to the people who are experts in that, rather than management or finance. He adds that the startup world will increasingly be ruled by technical people rather than business people. The idea of building something popular then figuring out how to make money from it was born in the Bubble. It sounds irresponsible, but it works.

If you can make something people want and not spend money, you're 90% of the way there. Startups will be ever more common because they're now so cheap to start. In most of the startups we fund, the biggest expense in the first year is simply food and rent. It costs little more to start a startup than to hang around doing nothing. And instead of having to go work in a cubicle in some office park, you get to work with your friends on your own project. If you succeed, you get rich. All part of the silicon valley edge phenomenon. Clearly, the web2.0 movement is gaining momentum - though the coverage seems to be ahead - calling for a reality check.In it own way the web2.0 ecosystem is beginning to be felt, albeit a small niche now. My feel is that these developments represent the very tip of exciting innovation to come — innovation that will require a new approach to venture investing led by a new breed of angel and venture investors that are able to successfully balance irrational exuberance with prudent funding to fuel the creation of new platforms for growth.

Norwest's Vab Goel finds that early stage companies in India are getting valuations at levels comparable to China. He believes that in India, there are not many true early stage companies & there aren't that many investment opportunities yet. The few that are there, are going to get big prices. As for later stage companies, the valuations are probably higher in China than in India China has taken multiple companies public on the Nasdaq; that has investors paying more.

In reality, as I have covered earlier, there is little or no real VC money available in India, as can be made available across various tech sectors(A limited number of online business related late investements are happening in india now). Companies that are receiving money in India are either spin outs from existing large businesses, captive units or second tier outsourcing providers that may lack the size or scale to compete with IT service giants and want the private equity money to grow through rollup and acquisitions. Investors find that in the early-stage investing business, there are a few small funds that are local to India but have not done too many deals and highlights venture money goes into early stage, pre-product or pre-revenue companies in the US , while a majority of the private equity is going into late stage businesses in India.

Courtesy of Rajesh saw this view on how failure breeds success. Breakthrough innovation - an imperative in today's globally competitive world, in which product cycles are shorter than ever - is becoming so extraordinarily hard. It requires well-honed organizations built for efficiency and speed to do what feels unnatural: Explore. Experiment. Foul up, sometimes. Then repeat.

Sramana Mitra listening Geoffrey Moore’s response on silicon valley’s future captures it : - Silicon Valley is very good at failing. Failing fast. Learning from failures. Using that learning to do new and different things. In any other place in the world, you get one chance, and if you fail, that carries a stigma for life, and you never get a second chance. Very powerful advantage. - The US still has the best higher education system. Great universities. - The US still has the most mature and best organized capital market. As of now the the silicon valley edge appears real. Today as I see it, in general most indian enterprises are hardly innovation chasing entities, and the framework for VC entry & exits are poorly defined. Coupled with limited VC activity in the past and archaic regulations – these make it a tougher breeding ground for enterprises like that of what is seen in the valley. VC’s and Angel’s may find it difficult to spot the next Flickr coming out of India. Angel investments and VC are so close to each other – the absence of one hurts the other very badly. The big company boards in India are mostly filled with family members and friends. The investor activism is very limited – the culture in general cascades across the ecosystem – the concept of family acting as passive investors leaving the running of the enterprise to professionals are quite limited in numbers and where in vogue it is mostly within well defined spheres of activities - in such cases direct compensations are better and not necessarily linked to sweat equities. Correspondingly the spark needed to work on innovative ideas aided by sweat equities for key employees second to many levels down mostly does not exist. The ecosystem inside India is also tough where job market dynamics at senior levels are less active compared to what we see in the western markets. The talent levels inside India continue to be very high – all it requires is a vibrant ecosystem - but not many recognize the issue here - talking india's growth for granted may be the biggest mistake - the country can't afford it. With all this , without doubt one hears in India- waves and waves of ideas for entrepreneurial moves in the tech arena – the spark, the ecosystem and the combination. The indian market shows propensity ot consume a lot many things. Entrepreneurs can spot many business opportunities therein as well.End of the day, its ideas, innovation, scale & speed of execution that matters more. As I wrote earlier, The US is the economic engineof the world – lets hope that it continues to innovate faster, better and emerge stronger. Collaboration in innovation is always a workable solution. Together with the Asia let more innovation blossom and let the world prosper a lot more - innovation and prosperity are closely related.

I wrote an op-ed piece for sandhill.com on the tactics for managing offshore costs.As it could be seen, with all of the excitement about the benefits of offshoring software development hitting the news over the past few years, everyone knew the "hype" pendulum would no doubt begin to swing in the opposite direction. And it has. There is mounting evidence that the bloom is off the offshoring rose, so to speak. Yet despite the challenges, offshoring remains a compelling option for many software companies. The vast majority of vendors continues to offshore and realizes significant competitive advantages for their companies. As their sophistication and experience with offshoring increases, many offshorers are seeking out new ways to control costs while retaining business value. The fact of the matter is that "lowering costs" is only one of many reasons why enterprises offshore work. Many experts say the key to deciding between outsourcing and in-sourcing is the overall differentiated value that outsourcing can bring. This takes into account the maturity levels of internal competencies - not for just today's needs but for maintaining a certain degree of edge in this dimension for the near future. That's one reason why offshoring studies find that even dissatisfied offshorers are as likely to continue offshoring in the near future as satisfied ones. When large enterprises leverage the global delivery model, the range of their offshore utilization increases. As this happens, the focus typically moves beyond back-room functions into more strategic areas of the business. In this way, the standard bidding process becomes a less preferred model for offshore vendor selection. Instead, more companies are realizing that their best partner is the one that offers them the greatest value - not necessarily the lowest cost.

The growth of offshore outsourcing has made for a hot Indian IT labor market - one of the main reasons costs for offshore resources are rising. The average salary increase is in the range of 15 percent per year. The reality is that there are multiple ways for customers of offshore service providers to better manage their cost equations:

- Have a Clear Plan - Increase Contract Length - Continually Re-evaluate On-Offshore Ratio - Continually Optimize the "Basics" - Employ a Shared Risks Model - Monitor Management Needs - Leverage Vendor Tools & Reporting - Employ a Shared Risks Model - Invest in Sourcing Advisory Firms - Adopt an Integrated Approach to Cost Management

Having said that,like in any other business, such strategies need to be dynamically re-evaluated as the business needs, strategies, models and execution methods keep changing. Clearly for the foreseeable future, despite the higher salaries experienced in India and other offshore markets, customers can continue to work with their chosen offshore service provider to maintain the cost advantage besides reaping a set of other known higher-order benefits in offshore outsourcing opportunities. Read the full article here.

Nick Dention makes an important statement – there's no doubt - there's a bubble now. The barrier to entry in Internet media is low," he said. "The barrier to success is high." While reflecting on this, courtesy of Shel Israel came across the piece about Indonesia's Defense Minister Juwono Sudarsono beginning to blog. Sudarsono's most recent post deals with efficacy in the new democracy. He writes, “The ability of the government, of private corporations and of all civic groups to make things happen and get things done rested on this single ability to energize government, corporations and advocacy groups”. Blogging is really catching up – at all levels.

Gary D. Halbert sees a disaster about to explode in the Chinese economy. In a well researched article, he highlights:

While it has become an article of faith that China's economy is booming & the economy is seen as growing rapidly- he points out that growth and size alone don't tell you how healthy an economic entity is. Chinese numbers are a paradox: Most analysts believe China's GDP is running at a 9-10% annual rate or higher. Industrial output in China surged 17.9% in the 12 months ended May. China's exports mushroomed by 25.1% in the 12 months ended May. Domestic retail sales soared 14.2% in the last year. Meanwhile, China's M-2 money supply exploded by 19.1% over the same period. In short, China's economy is out of control! He adds,perhaps worse, China is facing the threat of an enormous banking crisis. As the economy has exploded, Chinese banks have made mountains of loans to borrowers of all shapes and sizes, and today many of those loans are non-performing and will have to be written off at some point. The irony is that virtually all of the major banks around the world are heavily invested in China and have non-performing loans on their books as well. The problem is the massive overhang of debt, and in particular, troubled loans. Looked at from the standpoint of Chinese corporations, servicing this debt is a tremendous burden. Looked at from the standpoint of Chinese banks, the loans threaten the banks' viability if they become nonperforming. The solution of Chinese companies is to sell more products to generate cash to pay off the loans. It is difficult to sell into the Chinese economy because of high savings rates, driven by government policies and economic insecurity. The Chinese government needs a high savings rate to help stabilize the banks; dramatically increasing domestic consumption would undermine the savings rate, threatening the banking system just as surely as defaulting loans would. The solution for these companies, therefore, is to increase exports. In a world already saturated with Chinese exports, the only way to increase cash flow is to cut already low prices. That increases cash flow but does nothing for profitability. In other words, companies already saddled by debt burdens cut into (or below) profit margins to service the debt. Banks not wanting to declare bad portfolios arrange to lend more money to troubled enterprises. This allows some repayment of old debts, but simply puts off the day of reckoning on all sides (and increases the magnitude of reckoning when it arrives). Substantial portion of the loans disbursed by the Chinese banks this year is said to have gone to keep bad loans floating, like using one credit card to pay the monthly payment on another. You can do that for a while, but you can't do it forever.Thus, bank lending accelerates at a breakneck pace - not going into market-driven opportunities, but maintaining essentially failed enterprises for a while longer. Production surges at lower prices and the entire process moves faster and faster. For the Chinese government, Slowing down is dangerous and speeding up disastrous. China may be an economic and financial disaster waiting to happen. Virtually every economic indicator we see -- with allowances given for uncertainties in Chinese statistical methodology, to put it politely - is surging out of control.

Businessweek raises the question if google's fanfare and buzz meets with corresponding number of hits. The article notes,

Even if Google leads users to its new products, it needs to add pizzazz and improve functionality. Most areas it is targeting have entrenched rivals: For surfers perusing stock quotes, there's Yahoo! Finance. For chat addicts, there's AOL Instant Messenger. Those services have that elusive "stickiness" that makes users likely to return - for instance, often checked stock quotes already queued up in a finance site - which boosts ad values. With its huge market cap and lead in search, Google has time to work out the kinks and a culture committed to learning from mistakes. And it is collecting a wealth of data about what surfers want. Still, the message coming back so far is that if Google wants to live up to its reputation as the beast of Silicon Valley, it needs to search harder for products people want to use.

I had been writing for some time along these lines -look at the note on drilling good sense into google pricing. In a related note, I covered, while assessing non-search services & developer services one finds that Google does innovate in some spaces but has largely innovated in order to gain entry in markets that already existed. While google breathes innovation, competitors are generally quick to notice and are catching up its high time Google clearly explains its vision that it is executing for the next 2-3 years – very important that there should be a plan to grow and sustain the 100+Billion USD marketcap (incidentally bigger than the GDP of some oil producing Asian nations – the likes of Indonesia.) contrarian views about Google’s valuations definitely need a closer examination. I think this issue needs some serious evaluation as I had been pointing out for sometime like here, here about google's ability to sustain its leadership and support the very high marketcap. Google has to come out in the open about its plans for spending the money say building its own Internet, online index,along with monetizing models in more specific terms. True - some of google recent launches like Google Earth, Google Checkut may provide more monetizing opportunity - but where's the marketing and communication on those lines. I hardly see them.Its time that we get to see and know things beyond the likes of generic macro views like that of George Colony, which focusses only on what and not the how. Like in any other industry the responsibility of pioneers and leaders are lot more than just looking after themselves - they are trendsetters and role models in the industry.

Sadagopan's Weblog on Emerging Technologies, Trends,Thoughts, Ideas & Cyberworld "All views expressed are my personal views are not related in any way to my employer"