The Telecom industry is at the epicenter of the convergence phenomenon that we see in the industry today. It is always interesting to see them predict how the sweeping changes would impact business globally. Daniel Burns of Telstra’s Chief Technology Office, responsible for its Network Engineering, Fundamental Planning and Strategic Initiatives highlights a series of predictable developments. A few of them:

- In the office of the future, businesses will use a single broadband service for all their communications, including telephone, data and video services. Within that environment, wireless technologies will create an opportunity for businesses to provide employees with a lot more roaming capability. - Businesses will have a lot more management flexibility. New tools will enable businesses to update their systems, to do “adds,” “moves” and other changes to their servers much more quickly and easily than today. - IP Networks, moving voice and data communications to Internet-based networks, known as IP networks, will further reduce costs and create an opportunity for businesses to add new and exciting services. It will also provide enhanced security providing a very secure network to protect your information. Read the note Cisco'sIP Vision in the convergent world. - AI will really make it much easier for businesses to communicate with their customers. There is even the prospect of human-machine interfaces, incorporating communications tools into your clothing, or in your watch, to improve people’s health. There are just so many different things that are possible, and IP-based communications solutions are likely to play an important role in them all. - Wireless technologies are probably the most exciting area of emerging communications technology. Within the next decade, wireless networks will have bandwidth capabilities up to one gigabyte per second. This will create a huge opportunity for people to do almost anything from anywhere besides providing amazing mobility capabilities.

I wrote sometime back, Static productivity measures can be misleading & what may really count for enterprises is the ability to sustain and amplify productivity improvements through innovative products, process improvements or new business models. Unfortunatley most enterprises track static productivity measures so passionately and feel proud about it when lead indicators can present a dismal picture. A point that John Hagel emphasises in a related context. As he sees it, the rise of China and India can largely be traced to some very distinctive innovation being pioneered by companies in these regions.He points out that in the near-term, there’s a significant opportunity for all companies to harness these innovative management techniques to deliver more value to their customers.Kathy Sierra writes, risk-aversionis the single biggest innovation killer, and of course it's not just Microsoft that's been infected ( It may be noted Google is seen to be the opposite and hence the glam image). Taking risks is... risky. But if not taking risks is even riskier. Sure the big companies have it bad and may fall the hardest if they don't get a clue and a cure, but none of us is immune. You see the safe path everywhere. Her memo to Microsoft: you've got people doing some amazing things over there. If you could just get the hell out of the way, the world might change for the better. She offers some practical advice for individual nodes inside organisations: - Keep pushing the boundaries strategically, one-by-one If management layers are seen as conservative branches and leaf nodes are experimental individual contributors – the call is irrespective of being a leaf or a branch, pick your battles carefully, one poke at a time. Better to live another day to keep fighting the good fight then, say, being fired for trying to do it all at once. - Add one more skill to our career advice for young people: be willing to take risks! Perhaps more importantly, be willing to tolerate (and perhaps even encourage) risk-taking in those who are managed by you. A good read indeed - so much of insight embedded in simple words.

Recently we saw the revelation that Google built its own OS to manage grids internally. As we covered recently, Gmail was also an internal project used within Google before launched to the outside world. The Register scoops that Google is preparing its own distribution of Linux for the desktop, in a possible bid to take on Microsoft in its core business - desktop software. Dubbed, “Goobuntu”, a version of the increasingly popular Ubuntu desktop Linux distribution, and is based on Debian and the Gnome desktop. It reasons out that this could be for wider deployments on the company's own desktops, as an alternative to Microsoft. But it's possible Google plans to distribute it to the general public, as a free alternative to Windows. Google has already demonstrated an interest in building a presence on the desktop through Googlepack. Recent moves like this with Dell shows serious efforts in advancing this. However, entering the desktop software world would be a huge step. Making Goobuntu as easy to use as XP will require a lot more development. It's unlikely to be ready for showtime any time soon, and it's possible Google itself hasn't finalised where the project should go. Earlier, inquirer.net has called the bluff based on what was originally published here few months back. David pooh poohed the claim of USB based OS. Obviously Google has a lot of internal software written by it deployed for usage within – we have to see whether it gets eventually thrown open for public usage.But now its time Google outlines its vision in specific, trackable terms. Like in any other industry the responsibility of pioneers and leaders are lot more than just looking after themselves - they are trendsetters and rolemodels in the industry.

I am a resident of Singapore for a little less than three years now and I had been to this region several times prior to that. Singapore easily counts to be amongst the best cities to live and its infrastructure is amazing and the efficiency levels seen in the city-state in almost all day-to-day activities are unmatchable anywhere else in the world .Singapore airlines & Changi airport are modern day icons.I keep telling friends and colleagues that Singapore by giving the best of comfort spoils people in the sense – you leave the city – you feel as if you have entered into a world so inefficient in all possible ways. No doubt Singapore has invested in growth long before others in the region and to that extent the business environment today is quite changed –with size as a barrier probably one ends up mostly addressing incremental opportunities. Obviously a very tough but a dynamic environment lay here – intermixed with its squeaky clean image singpore looks amazing any whichever way one looks at it. Singapore is just not known for what it has achieved but for its ability to continually keep moving –mostly pushed by the government, amongst the smartest one of its kind in the world. We just came back from sentosa – a place that am visiting aftet two years – my wife told me that everything therein looks changed. Paul Greenberg appears completely bowled over by Singapore’s focus on service excellence. He finds that its not often you find an entire nation committed to the improvement of service that is clearly focused around the experience economy. It is an opportunity to see how entire nations can devote public services with a commitment from all its citizens to achieving what we've all been trying to do. Let's watch this one closely. We got a real chance here to help make something of something that is already being made. I earlier wrote about singaporetopping the global IT readiness index – Singapore amongst other things is seen as the best performer worldwide in a number of categories - quality of maths and science education, affordability of telephone connection charges, and government prioritization and procurement of ICT - and gets extremely high scores in other areas, such as affordability of Internet access. Singapore infocomm development authorities ten year IT plan is unarguably amongst the best of its kind. Singapore’s competitiveness and dynamism is undergoing a huge change – Lot of initiatives are being tried. The remaking Singapore report is a shining example of citizen involvement in shaping government policies.I can relate to most of what Paul writes – several of the institutions and some of the people referred in his article are known to me – I can only say that all these are correct impressions. Ofcourse like anywhere else there are different shades of colors that one could experience, but on balance, the city-state with a population of three million which has amassed a reserve in excess of hundred billion dollars is a real marvel – the beauty is it is trying to improve further.

Engadget reports that both Gates and Microsoft CTO Craig J. Mundie talked up the idea of a specially designed smartphone that could be connected to a TV and keyboard, turning it into a full-fledged computer. Mundie highlighted that everyone is going to have a cellphone. Come to think of it, the cell phone is the platform as against the laptop – the no.of cellphones exceed the number of laptops,potentially at about two billion people with each other. Some concerns about the service provider knowing all the content indeed exists – but what would one do with so much of content.Google also seems to recognize the increasing importance of mobiles. Google talk is now available for mobiles. The key thing to note here is that both require that huge infrastructure like electricity , communication be setup prior to this happening. That’s another impetus for expediting setup of infrastructure in developing nations. This could direct question the model of the low cost PC's

Philip Greenspun was amongst the early proponents of the idea of making mobile phones as home computers. As he sees it, a mobile phone has substantially all of the computing capabilities desired by a large fraction of the public and he raises the question,why then would someone want to go to the trouble of installing and maintaining a personal computer (PC). Evidence this can work: Millions of Japanese consumers whose only home computing device is an iMode phone, providing them with text messaging, Web pages, and various social and commercial services. Pointing out that the combination of the phone and appliance is more powerful than a standard PC in some ways, typical uses could be things like : The physical phone plus a PIN number serves as a secure key identifying the customer and a means of billing the customer, as being tried in Japan and parts of Europe as a payment method in shops, for vending machines, and in dealing with government. Someone engaged in online shopping with the phone/Appliance combo should not need to enter credit card data, shipping address, etc. every time he or she buys something. Similarly subscription services can be added to and dropped from the customer's phone bill without the customer having to remember additional username/password combinations. I agree that the best way to push through this problem is to make the Appliances free or very low cost with a service agreement, the same way that carriers have managed to sell hundreds of thousands of expensive smart phones.

Topix.net’s Rich Skrenta writes on the right approach towards citizen journalism. As he sees it, the key to understanding what is working in "Citizen Journalism" is that they're first-person accounts. Journalists are professional observers and interpreters; they watch, and report back to the wider audience. But just like stockbrokers and travel agents, the Internet is again cutting out the intermediary. The best examples of CJ, such as Jeremy Hermanns reporting on a cabin depressurization on Alaska Airlines or things similar to the ohmy news phenomenon.

Some points that he makes are excellent read : "The quality of journalistic output today is, for the most part really really good. In fact it's too good. The product costs a huge amount to bring to market, and what the Internet enables is a an alternative product built for zero, and providing a different value proposition. Citizen journalism is going to be more Citizens and less Journalism. " and "Creating a local news page for every town in the US provided us with a set of local audiences for thousands of towns... towns where people who use AOL and have never heard of Web 2.0 live. These people want to tell their stories too. You don't need to know what a blog is to want to tell your story online, and you don't need a journalist to tell you how either, it turns out." Good read.

SAP opines "India is slowly getting expensive" ,and that SAP has decided to hire a certain number there, and then start looking at other locations. Reportedly Kagermann pointed to India's relatively high staff turnover, which is fueling personnel costs & SAP is likely to expand in China and Eastern Europe. Some called me to know my view how service companies tend to look at this.(Like all other posts, I speak for myself like all other posts here and is not anyway related my employer's views). I had recently written China Resource Scaleup Disappoints India Headquartered Companies!! Recently we covered China no big force in software services and covered the Mckinsey perspective on china's software sector, it will be many years before china poses a threat to its continental rival.We also covered the point of view that its going to be the Indian Headquartered companies all the way in future ruling the IT services market. Financial Times recently wrote, China is far from the promised land for Indian software service giants. For service companies, In particular, there is a lack of suitable local applicants for jobs as project managers and quality control managers. In India, such people, typically with 5 to 12 years experience including stints in the US, are paid premium salaries. Software companies are forced to send project managers from India to Shanghai, raising the operating costs there. A lack of bilingual Chinese IT professionals, for jobs such as team leader, is also holding back expansion. One English and Chinese speaking programmer is required to oversee a team of four local developers who speak only Chinese. Because there is only a small number of bilingual programmers, they can command a salary premium of 30-40 per cent. These labour market deficiencies have not gone unnoticed among customers in the US, which is the biggest market for Indian IT. As I mentioned, China : No Big Force In IT Services,Its India All The Way. But I recognize that SAP could be looking at personnel of different profile – essentially to work as part of SAP’s engineering/testing. SAP is also very big in china – it is the largest enterprise vendor in china and therefore it may make sense for them to stay invested lot more in the mid kingdom. To attribute that expansion may not be in my view entirely correct – most of the Indian engineers would like to be part of a job which would help them travel outside India – most of the western companies – product & service companies included are yet to realign the model to meet this basic aspiration – that’s actually preventing them to scale up in great numbers as against good numbers. In my view, already SAP is big in India, but it may be unfair to name India as expensive compared to china. A recent Mckinsey report found the attrition in china at about 20 percent, compared with an average of 14 percent in the United States(Indian average for IT biggies may be similar), which itself has a very fluid IT labor market. Accenture recently reported that its global attrition level remain at 20%. Look at Oracle's India Plans. I would think that investments in various locations are in general mutually exclusive events, so long as things are not shut down in one location and corresponding rampup happens elsewhere.Also just a thought -lot better things can be accomplished without making press statements!!

I have read years back Hal Geneen proclaiming that ITT as the CEO university. Its another matter that the conglomerate almost fell apart after his tenure. This is an interesting list of companies that produced the most chief executives – I have seen companies calling their key executives as CEO’s in waiting and some companies pride themselves as a company of CEO’s. There are some companies where every executive behaves like a CEO & there are companies where CEO does not matter & there are companies where CEO’s are everything – new economy or old economy does not matter!! There are companies where everyone likes to imitate the CEO behavior. I normally watch closely what happens to an enterprise after the CEO departs giving a true result about the effectiveness, much before the new CEO is able to bring in changes/stamp his imprints across the organization.But anyways an interesting list - Have always found CEO’s coming from deeply talent rich companies doing well – atleast the ruboff effect used to be pronounced. I have generally seen new CEO’S after taking charge driving change as change agents bringing huge difference to the DNA, Culture and ofcourse results. We have to grant that it is an incredibly powerful combination for a dynamite like CEO groomed in great instituitions (important that he /she does not get trapped in the comforts of the office).

Following the keen focus planned on India , Manjeet Kripalini finds Indian top ministers and policymakers making many lucrative contacts among the foriegn power brokers on hand at the global economic conference – the high and mighty skipped annual jazz dinner at WEF to attend Indian cocktail. India has been helping itself quite effectively at Davos this year as can be seen by overflowing India sessions – late nights to early breakfast meets et all. Ministers acted like salesmen, high level bureaucrats wined and dined with global business leaders, Japanese big investors actively wooed for infrastructure investments. India actively talked about the 10 paradigm shifts taking place simultaneously in India – besides outsourcing, the country is now focusing on becoming a manufacturing base, largest middle class in the world, largest english speaking population on earth, the youngest nation with fortunate future demographics, all very attractive for global business. Indian industrialist have provided a matching visibility & support for attracting investments. India now needs an action bias – groundswell of interest can dissipate if nor converted into stretchable filed level pops – India is generally seen as slow in execution and in finalizing policy level decisions – delays in decisions related to airport modernization, all need to be stamped out with firm determination. Delhi Metro, Konkan rail lines – all have shown that India can deliver – obviously we need hundred of such new cases to report year after year. As Klaus Schwabdescribes, India needs to make further improvements in four important areas. - The first is in education where the needs are particularly urgent at the primary and secondary level. Where tertiary enrolment rates are low, the scope for improvement in girls’ education is especially broad. - The second is infrastructure; India needs to improve the quality of overall infrastructure, including roads, ports, airports, telecommunications and power generation. - The third area for improvement is the extent of bureaucratic red tape and regulation – ensuring a favourable environment for business, especially entrepreneurship. - Finally, India needs to continue to address its fiscal deficit problem, both its public debt level and its revenue collection.

During my visit to China last fortnight,someone told me that Shanghai city has more cranes than the combined number found anywhere else in the world – I am not sure of the veracity of this – but the effect is real. Let thousand and thousands of cranes crank, let decisions be made faster, let the execution of these engagements make record of sorts for execution. Let the slogan "No To Inertia" get more and more heard - clealry there is a huge chance to make a bright & better future for millions and millions of people lay there.

Despite initiatives like this, concerns of privacy intrusion owing to RFID technologies abound. At one end views as vitriolic as RFID tag activated bombs exist where some think that given the one way trust nature of the protocols, where the RFID tag betrays vital information to any reader device, promiscuously, there is no reason why terrorists or military opponents could not easily target individuals or groups of individuals with landmines, booby traps etc. based on the RFID tags which are detected on a person e.g. a bomb which only kills rich American or European tourists or singles out military personnel from the local civilian population. The current plans to include contactless RFID chips in, for example, the new USA Biometric Passports, without any encryption at all, will lead to easier automated target reconaissance for terrorists, who will no doubt program a bomb to wait until several US Citizens are within range before detonating itself automatically. Bruce Schneier points to an excellent cartoon by David Farley on RFID , Privacy Intrusion & Packaging. It says it all.The industry’s response is very limited – they are also struck by the frequency regulations across the globe – but to be fair privacy intrusion are only a limited dampener in the adoption of RFID – Some high voltage showcase success is what the industry needs now – Beijing Olympics may be that –that is a few years away - but obviously lot more needs to come from the western world.

Michael Moritz of Sequoia, the NO.I in the Forbes Midas List says that consumer-tech businesses, are a pit of "muck and mire." As he sees it(after making tons of money out of it recently), they have low margins, require massive marketing budgets, compete with monster retailers' house brands and face Asian copycats. Though he has helped fuel the consumer craze, he laments the rise of handheld gadgetry: "The march of consumer technology will spell an end to tranquility & warns that most of the venture money going into consumer-related companies will be squandered, and the rest will be lost." David Chao (10)and Dixon Doll (24) were among the first U.S. VCs to woo middle-class shoppers in Asia. This year they took five firms public in Asia, including JCI, a wireless provider. Says Chao:"If there is any one engine that is going to drive the next bubble-good and bad-it will be those billion handheld devices that will be sold in 2007." Forbes notes that a lot of names on the list last year are gone with the disappearance of the gargantuan valuations of the boom era. The article also notes that with the continued rise of China and India and waves of driven, newly minted capitalists, these rankings will get more multinational each year. It is no coincidence that all the top five dealmakershave been associated with Google in one way or other. The list of sectoral interest, polled by readers,actually surprised me - by and large looks lot more balanced.I hope to see the oversee investment share move from 20% to higher number in the years to come.

Listening to the podcast of a powerful panel on digital 2.0 in the world economic forum titled, the future of the technology sector, the panel chaired by Geoffrey Moore with participation by Bill Gates, John Chambers, Eric Schmidt & Niklaus Zinnstorm is a dream come true –perhaps the best panel that can ever be assembled. While we have earlier covered the big bang effect of digitization, the discussions in the WEF panel clearly took things to a different plane. Geoff Moore set the framework for discussions on two fronts: - Technology issues now transcend technology companies and are now nearly all pervasive across the industries & sectors. - Gordon Moore’s law predicting technology capability improvements 10x to 100x improvements in about 5-7 years is probably losing what Geoffrey calls as its exploratory power whereas the impact of the internet is shifting( read my note on the impact on enterprise software )the focus towards service models – this means that Moore’s law is still relevant but more or equally powerful other forces are shaping the growth of the tech industry and by extension all industries & sectors. What followed was one of the most illuminating discussions about the future/opportunities that technology would be creating for the business/society in general. Some of the points that came out in the discussions: - Bill Gates who was invited first to talk, spoke about the almost near zero cost of computing, storage and bandwidth and admitted when asked about aligning Microsoft to the changing reality that catching up in some areas is also an important strategy that it follows while trying to create the future in the PC related arenas. - John Chambers came with the notion that the shift now is from transactions to interactivity bringing about huge increase in productivity and means to reaching and delighting customers - Eric Schmidt spoke about the how the various tech advances have really come together and created a perceptible critical mass – redefining rate of growth in driving new markets and new business segments. His point of increasing rate of adoption & the dawn of new service models creating new customers was quite insightful - A point that Niklaus Zinnstorm built on – Skype has built up a customer base of 75 million in 3 ½ years & pointed out that ARPU costs are not relevant and the only the ecosystem mattersmore as the incremental cost of scaling up is virtually zero. - The new metric now becomes the ratio of active users vs customers( right now it stands at single digit ) – this is applicable to Skype, Google & Microsoft as well. - Eric Schmidt drove the points out the shift from technology enabling strategy to technology driving/determining strategy in the emerging world. - As the internet becomes so ubiquitous and stable and with integration technologies getting simpler and open, small companies/startups anywhere in the world can focus on a chosen thing and create a huge impact – this is really a phenomenon that we shall see increasingly become significant in future. Talking of ubiquity of the internet, Gates added, "with ubiquitous connectivity “you can eventually even get rid of telephone numbers". - The impact of all these in the business model changes across industries is what John Chambers highlighted, one that would be increasingly felt and amidst all these things what about the telco’s who have invested in the infrastructure wanting to get a share of the new pie – while John felt that net-net bandwidth shall become free and Bill spelt out the infrastructure players shall focus on new biz models centered around video rendering and related services opening up a new revenue stream. More is available in the podcast that includes Microsoft’s/Google’s digitization strategies. - A lot more insightful, interesting and humorous discussions followed In a nutshell the conclusions veered around: - Free infrastructure- computing,storage & bandwidth - More value shall be derived from IT enabling transactions to enabling interactions - Digitization of all possible things, and make them available over the net – this would push for greater value creation through related services. In Dealing With Darwin, Geoff Moore outlined the need for companies to innovate in various phases of its evolution, here he has more or less set the tone for the need of the business ecosystem to focus on the need to innovate and adopt in its evolution as well. Clearly the vision, readiness, availability and early success /demonstrations are happening - the key would be to see how things rapidly/deeply/innovatively shape the various business around the world in the Digital 2.0 world.

Subir Roy writes the story of TCS, Wipro & Infosys – He relates to these as three chickens which all laid eggs - One was shy, one was honest and one was a chicken with hype. All laid an egg each, ordinary looking, whose product quality was identical, say 100. The first made a noise of two decibels, so very few heard of it and came to see it. But with those who did come, it scored 98 plus. The second was the honest chicken. Its product quality was 100, it made a noise about being 100. Everybody came expecting 100, got 100. The end result was even or neutral, neither positive nor negative. The third chicken, whose egg was of quality 100, made a noise that it was 400, everybody came expecting 400, but got 100, that is minus 300. If you have not guessed it yet, the first chicken is Tata Consultancy Services, the second is Wipro, and the third is Infosys - the three leading lights of the Indian software industry. The three represent a fine conundrum. For the record, I disagree with the rankings or the comparison made in such narrow sense.

My Take: The article while recognizing the different marketing strategies these employ makes the claim that they offer near-identical services of near-identical quality and there is little to distinguish them in the way they meet customer requirements ( This is a myth – increasingly the offerings and depth or lack of it are showing up and look at the vertical revenue distribution/service offering revenue amongst these companies ). This is an excellent article – while there may be some misrepresentation of facts , the article is highly insightful – never have I seen something published like this with so much of detail – while being an industry insider with so many contacts and interactions – we get to know all these and perhaps a lot more but for someone not interacting with these companies – a highly recommended read about the major players that were mostly instrumental in changing the rules of the game.

Matt Marshall writes about the latest venture of two of the founders of Junglee: Anand Rajaraman and Venky Harinarayan : the duo have come together to launch Kosmix. From siliconbeat : "Aiming to what they call as unsolved problem on the web - they are making an audaciously risky bet that they can crack the code on a vexing problem in search: finding the meaning, or at least the topic of a Web page. Kosmix is betting its deep technology can help improve upon Google's one-size-fits-all approach for many types of searches. Google may work well when you're looking for a specific answer.But what if there's no one right answer? This is where Kosmix wants to help you, by searching the entire web and narrowing the results to the particular area you are interested in - and then giving you a choice of answers". The duo claim most of these other sites crawling only 500 or so Web sites relevant to their niches. Kosmix, like Google and Yahoo, is crawling and indexing the entire Web. It has come up with its own technology to rank pages by category, instead of by keyword. Kosmix doesn't use pagerank - or popularity, based on the number links to a page. As pagerank is seen as inefficient when it comes to categories. Instead, Kosmix looks at what pages that link to other pages are saying - to take a bigger stab at judging the meaning or subject of the page. Its like the "category rank" - essentially tagging pages with categories- call it "Auto-tagging the Web." There are some interesting anecdotes as well: Post jungle.com acquisition by Amazon, they worked for a while in amazon.com and Rajaraman shares an interesting detail – when approached for an acquisition by amazon – he recalls: "And we kind of asked, at that point, 'Sergey, if Amazon were to buy you guys, what sort of price would you sell for?' I remember Sergey telling me: 'The only kind of price we'd accept would be something with ten digits [billions].' If he'd said nine digits, we might have talked." Kosmix has started with a health search, but will soon roll out travel and politics search, and will follow with a rolling thunder of scores of other types of searches. This is not lightweight stuff. They have filed patents, and there's tons of math in their algorithms. Interesting to watch – trials returned interesting results.

Chris Anderson makes a good case to look at the current movement in the tech worlds as a boom and not a bubble. As he sees it three reasons are driving this: - First, technology adoption has continued at a torrid pace (and even accelerated at times) despite the bust. The digital-media boom sparked by the iPod and iTunes has blown through even the most aggressive forecasts. - The second reason is that the sunk costs of the dotcom era make the economics of entrepreneurship more favorable. We're now enjoying supercheap bandwidth. So, too, for storage, screens, and a host of other technologies that are benefiting from profligate '90s-era investment and research. - With reducing prices – read this - one can can start a company today for a tiny fraction of what people spent five years ago. In this new environment, startups can grow organically. That means less venture capital is needed - and that's the third reason this boom is different. So there you have the recipe for a healthy boom, not a fragile bubble: a more receptive marketplace, lower costs, and lighter pressure from investors, argues Chris. I definitely see an upswing in activities in the market, though enterprisewide adoption of new technologies look weak.Anderson captures the new dynamics in vogue governing the techworld.The key thing would be to see how to make this broadbased – for example, opensource foray into the enterprise is very limited, the promised internet’s disruptive effects , all need to happen now. The role of the investors can not be underemphasised from the supplyside and this should be felt at all happening places in the world like in india, fast becoming the technology epicenter. At the same time periodic checks that good sense prevails need to be taken. There is also an acute need to make enterprise scale changes happen in the industry to sustain the momentum - one that can provide measurable vaue to business.

Recently I wrote that Google inside enterprise would be a n interesting thing to watch – to recap, I wrote that if Google expands its footprint in the enterprise space - e.g., to develop content management or authoring tools - it will come as a hosted service or (like its enterprise search product) an appliance. Recently, EMC and Google announced an agreement to integrate EMC Documentum Enterprise Content Integration (ECI) Services and Google Desktop search.Recently EMC’s software integrated both Google.com and the Google Search Appliance, letting customers leverage Google’s search products as information sources. Frank Gens predicts that in the near future many enterprise vendors shall begin to court Google aggressively. In his schema,Google would provide the Web platform with its existing, massive, computing infrastructure of hundreds of thousands of servers around the world. It could team up with a whole array of companies to actually write applications — from information and content management to business analytics—on top of that platform. It can be seen that Google is stepping into the world of enterprise and this can be seen as a precursor to Google focussing its energy in the enterprise software sector as well in the days to come. Frank points to Google having similar agreements with IBM and Sun as well, but as I see it should also be noted that EMC dumped verity as the choice search player last year and is now embracing Google – clearly the Google brand is having a good pull. This is also a precursor to consumer technologies setting integrated under the hoods so to say in the enterprise landscape. Since individuals are getting so familiar with Google, coupled with its versatility, it is pushing enterprise players to court these products more aggressively. Pervasive devices usually associated with individuals are long getting integrated into the enterprise space – mobiles, blackberry’s, VoIP applications etc. Frankly I do not attach great importance to Google moving into the enterprise space as earthshaking – there are far better enterprise players in the fray there – specialist players offering superior benefits. Google can play the game of being inside enterprise space- that could be the only disruptive influence therein. It should be noted that the best enterprise search player is seen as Vivismo and not Google. Also it need to be noted that press releases are just that and need not become a centerpiece strategy in occassions like this. EMC seeing itself as the winner in the ECM space, would like to broadbase its appeal and this should be seen as a step in that direction. I genuinely believe that one of the reasons that EMC wants to play the Google card is to hedge against any potential acquisitions that may affect the other search players – the space is beginning to see some consolidation of late (Verity got snapped by Autonomy in a surprising move recently) With IBM & Oracle failing to make any significant dent in the enterprise content search space,tomorrow can be anybody’s guess - so it is prudent to have a strong neutral player as part of your ecosystem and that I suspect is the biggest reason for this coming together – a good move indeed on the part of EMC - but I refuse to see this as a trend wherein google could move in to storm the enterprise market.

CEO departures normally precede/succeed bad developments inside an enterprise. Tony Byrne wonders how come when both Interwoven and Vignette announced improved results ,their CEO’s are headed out. Hopefully these two vendors are not getting acquired. Vignette's Thomas Hogan is moving on to HP Software (HP was always rumored to be on the lookout for acquiring a content management vendor & an EAI vendor), while Interwoven's Martin Brauns is retiring. Pointing to decent Q4 earnings (Vignette, Interwoven),& rounding out successive years of steady but very modest growth is indeed a respectable accomplishment. These two companies have withstood the onslaught of the bruteforce consolidation and stood their ground. For a quick comparison, look at the state Broadvision is in today – once it used to be revenuewise bigger than these two players put together. Let’s hope the change makes these two companies much better.

The change in the BPM world is dramatic : from process modeling & workflows the framework has improved to support all aspects of the business & digital world across the process. This provides for a tight intrlocking of desired actions to real results BPM suites combine process modeling, execution and performance management in a coherent set of software tools linked by a coherent management philosophy. Because it is neither IT infrastructure nor an enterprise application, BPM is still not well understood by IT. Instead of treating business modeling, IT implementation and performance management as independent endeavors, BPM unites them with an integrated set of tools and an overarching management philosophy of continual incremental improvement. Naming five reasons to invest in BPM, Bruce silver lists them: 1. Simplification – Documenting current process architectures and analyzing them for simplicity & efficiency constitute the bulk of BPM engagements 2. Efficiency. Efficiency improvements are the No. 1 source of return on investment from BPM. 3. Compliance and Control. BPM ensures compliance not only with policies and regulatory requirements but also with best practices tuned to performance objectives. BPM tools encourage reuse of process fragments throughout the organization while allowing local variations where they make sense. 4. Agility. Through orchestration, services get interconnected & render themselves to be modified quickly in response to changing demands. 5. Continuous improvement. Like corporate performance management systems, BPM supports high-level strategic metrics, drill-down analytics and alerts when results begin to deviate from performance targets. BPM can turn alerts into automated real-time escalation and remediation procedures, providing zero-latency response to the business environment. Ultimately, parameters distilled from actual operations can be fed back into the process model to begin the next cycle of performance improvement.

My Take:The BPM space winners are surprisingly not the big players but the best-of-the breed lot. It is time that we begin to recognize the players based on their capabilities and general strengths and not necessarily look at the big players for all types of solutions – Big players need to be grilled a lot more in their ability to provide emerging cutting edge solutions on specific niche areas– while they may be the starting posts for any enterprise procurements – as things evolve it may become the case that they may not be seen near the end posts in evaluation post everytime. Therein may lay the solution for the growth of the enterprise software sector and the ability of business to overall extract better value from IT. Bryan Stolle once wrote there is still much innovation to be done, especially as the market gets more and more vertically focused. With the current moods however many innovative vendors will have to shut their doors before they get the chance to be the next Salesforce.com. Big vendors also need to begin to get measured on new parameters like innovation /innovation absorption, to ensure that they stay along the curve of progress. As I wrote recently I do not see how the large platform players can do away super special players( there are many of them - some have existed for decades - though a majority of them for just under a decade) or provide justice with specialized smaller companies like rules engines, collaboration systems, content management systems, document management systems, procurement solutions, business intelligence etc. Clearly there shall be several smaller companies that would co-exist as part of the larger enterprise ecosystem. Big vendors may not be the only choice for connecting all the dots in enterprise space(while unarguably they shall hold the central place there) - other specialist/niche players also hold a legitimatley well earned space - the sooner this is understood and get reflected in thoughts and actions - the better it is for the complete enteprise ecosystem - without further straining the already near fatigued corporate buyer sentiments.

Vinnie points out that while we use and enjoy Google, Yahoo and Apple products, most of us work with and professionally appear more interested in enterprise technologies and vendors. He says that he is almost on a crusade to see more blogs written on enterprise vendors and topics like telemetry, biometrics, BPO, SaaS - not just consumer technologies and web 2.0. He is spot on when he points out that the enterprise spend is over 10X the consumer spend, but the overall attention of media and blogs appears the inverse. I do write about personal/consumer technologies, partly because there are more regular developments and the pace of change is faster but enterprise technology is close to my heart and clearly it has much larger impact on the society as a whole. As Dennis Howlet points out we have to play the game – otherwise in the memeorandum model, enterprise blogs get subsumed. Whats the game like – when I mailed Gabe a few weeks back and asked for a clarification – promptly he wrote me back - Every night the process described here repeats: http://blog.memeorandum.com/050922/whos-included and he recommended you link a lot and strive to get linked to make sure the blog surfaces in the tech filter. Addressig my concern of recent posts not surfacing in tech memeorandum , he wrote that if you appeared regularly before but not now, it's probably because some posts of your got some attention earlier but not recently and suggesyed that I post some more things other people link to you're likely to show up again... I found the logic a little strange!! On a related note,it is also deplorable to see that for the American media/aggregators/filters–blogosphere included, the rest of the world does not matter – barring a few exceptions. Its time that a movement called enterprise blogs get noticed in the expanding blogosphere.

While many are closely watching the Google Vs Federal Govt issue & Google's decision to acceptchinese censorship, perhaps we overlook how even our personal data that we keep with us are sometimes vulnerable for others to potentially misuse. The venerable Bruce Schneier writes that it's now amazingly easy to lose an enormous amount of information. In the article that appears in the Wired magazine, he points twenty years ago, someone could break into an office and copy every customer file, every piece of correspondence etc. Today, all he has to do is steal a computer/portable backup drive or copy all data, and one would never know about it. With miniaturization and proliferation of small devices in this increasingly digital world, If anything, this problem has gotten worse. The digital devices have all gotten smaller, while at the same time they're carrying more and more sensitive information. The laptop could easily contain every e-mail sent and received over years, and may contain , an enormous amount of work-related documents, and all personal details. USB’s normally carry so much of backup data. Blackberry’s & Treo’s contain all email info, phone numbers and a detailed log of phone calls made/received. He offers two possible solutions: - The first is to protect the data. Hard-disk encryption programs like PGP Disk allow encryption of individual files, folders or entire disk partitions. Several manufacturers market USB thumb drives with built-in encryption. Some PDA manufacturers are starting to add password protection - not as good as encryption, but at least it's something - to their devices, and there are some aftermarket PDA encryption programs. - The second solution is to remotely delete the data if the device is lost. This is still a new idea, this may gain traction in the corporate market. Important aspects that end consumers should focus on and push the manufacturers/service providers to share.

Seldom do I get the time & patience to look at projects in the academia( no disrespect meant – its just that I do not find the time to look at them – being choked in the commercial world for a long time!!) –Some friends shared the information about the new internet related efforts. The GENI (Global Environment for Network Investigations ) is an experimental facility being planned by the NSF (with an outlay in excess of 350 million US$), in collaboration with the research community works with the goal o enable the research community to invent and demonstrate a global communications network and related services that will be qualitatively better than today's Internet. The belief is that if the Internet is going to deliver increasing value to society, then experimental facilities that allow the research community to address new threats, exploit emerging technologies, enable new applications, and foster the embedding of the network throughout the physical world needs to be fostered.

-The Internet is not secure - with worms, viruses, and denial of service attacks, and there exists enough reasons to worry about massive collapse, due either to natural errors or malicious attacks. Problems with “phishing” have prevented institutions such as banks from using email to communicate with their customers. Trust in the Internet is eroding.

- The current Internet cannot deliver to society the potential of emerging technologies such as wireless communications. Even as all of our computers become connected to the Internet, we see the next wave of computing devices (sensors and controllers) rejecting the Internet in favor of isolated “sensor networks”.

- The Internet does not provide adequate levels of availability. The design should be able to deliver a more available service than the telephone system. In particular, it should meet the needs of society in times of crisis by giving priority to critical communications.

- The design of the current Internet actually creates barriers to economic investment and enhancement by the private sector. A large number of specific problems with the Internet today have their roots in an economic disincentive, rather than a technical lack Besides highlighting a few more limitations, the report points out that these limitations are deeply rooted in the design of the Internet. It is easy to overlook them because of the astonishing success of the Internet to this point. we may be at an inflection point in the social utility of the Internet, with eroding trust, reduced innovation, and slowing rates of uptake.

While the current looks like this, the future Internet must enable and encourage: - A world where mobility and universal connectivity is the norm, in which any piece of information is available anytime, anywhere. - A world where more and more of the world’s information is available online—a world that meets commercial concerns, provides utility to users, and makes new activities possible. A world where we can all search, store, retrieve, explore, enlighten and entertain ourselves. - A world that is made smarter—safer, more efficient, healthier, more satisfactory—by the effective use of sensors and controllers. - A world where we have a balanced realization of important social concerns such as privacy, accountability, freedom of action and a predictable shared civil space. - A world where “computing” and “networking” is no longer something we “do”, but a natural part of our everyday world. We no longer use the Internet to go to cyber-space. It has come to us. A world where these tools are so integrated into our world that they become invisible. Good project worth monitoring for progress.

As we covered earlier digitization does not respect any defined categorization such as tech or consumer electronics. We are now seeing a collision of three massive industries Viz. the computer and software biz( US dominated),the consumer electronics sector(Asia centric) & telecommunications industry( across the world). All three groups will have a hand in building the digital wonders that are headed our way. Paradoxically, none of these industries, much less a single company, can put all the pieces together. As this article points out, convergence used to be a much talked word in the past – but most saw some combination of television, computers and an intelligent network that would give consumers much more control. Today, Video is popping up on cellphones, iPods, TiVo's and Web sites. And as for blogs, photo-tagging sites like Flickr, podcasts and the rest of the bubbling digital stew, it's clear that lots of media are coming together in lots of devices in lots of ways. This convergence spells trouble for many established companies. The anything, anytime, anywhere paradigm is really going to shift the world of media. Old-line media companies' fears can be lumped into three nightmarish categories: - Business-model anxiety : Newer services like Apple's iTunes, TiVo's Video from advertising-supported Web sites, Bit Torrents all these are questioning the notions of existing models. - Creative anxiety : With facilities for production of any combination of video, text, sound and pictures for viewing on a 50-inch TV, a laptop computer or a cellphone screen. conventional media is getting increasingly puzzled about how to counter the onslaught. - Control anxiety : With weblogs and the rise of online communities, commoners can be distributing podcasts and movies online on their own. The career prospects for hit makers, gatekeepers and even fact checkers may well be in doubt.The internet has broken down the barriers & accelerated the development of new solutions like efficient ways to deliver high-quality video signals. The primordial soup of more bandwidth, more storage, more devices and more people creating content which is inherently digital, is inherently very powerful and the speed of absorption has alighted ahead of the studied response of the old media. Covergence is cutting through the sheath of tradition of invincibility.

Courtesy of Howard saw this well compiled note titled internet ties. The report submit that the internet is reinforcing new set of ties in the society & that this would improve over time while reaching larger masses. The internet has become part of everyday life. People routinely integrate it into the ways in which they communicate with each other, moving between phone, computer, and in-person encounters. Instead of disappearing ties, people’s communities are transforming: The traditional human orientation to neighborhood- and village-based groups is moving towards communities that are oriented around geographically dispersed social networks. Today people’s networks continue to have substantial numbers of relatives and neighbors — the traditional bases of community — as well as friends and workmates. The internet and email play an important role in maintaining these dispersed social networks. Rather than conflicting with people’s community ties, the authors submit that the internet fits seamlessly with in-person and phone encounters. With the help of the internet, people are able to maintain active contact with sizable social networks, even though many of the people in those networks do not live nearby. Do not miss out the section on the role internet plays in taking decisions. A must read report if you want to taste a sample of the profoundness of the report : Even though there are fewer people contacted, they are a greater percentage of your network. This pattern - the percentage of one’s social network contacted declining as network size grows - holds true for almost all forms of contact analyzed in the Social Ties survey. The one exception is email. As the size of people’s social network increases, the percentage of one’s social network contacted weekly by email does not decline but remains about the same at about 20% of core and significant ties.

The title of the post says it all. Wired News has a story about the impact of DRM on the future of the digital entertainment industry. The article brings up some excellent points about the effects of DRM in bringing limitations on innovation within the industry.This year may be the year that gadget makers finally conquer the living room, replacing DVD players, VCRs and personal video recorders with all-in-one media devices that serve up HDTV, pre-recorded movies and digital music. If so, it will likely also be the year that people learn the meaning of DRM, an acronym the industry says stands for digital rights management, but critics say should stand for digital restrictions mongering. The key players in the CES market for whom DRM is highly relevant look at it more as a problem than a solution and hence come out with suboptimal means of enforcing DRM. Google, generally recognised for doing things right recently came out with its own DRM standards, adding to the complexity. While on this do not miss reading this.I agree with cory doctorow’s view that technology companies will eventually decide that entertainment companies' demand for DRM is hurting their bottom line & that’s when truly innovative gadgets will become available. Clearly doing less with more and more powerful gadgets will not go well with the masses.

(Via Economictimes) In what may be seen as the second largest deal in the local software services sector, slightly smaller than the $593m Oracle paid to acquire Citigroup’s stake in banking product company iFlex, it appears that EDS may buy out Mphasis. The total acquisition cost may be around 1600 crores. It is said that EDS is likely to not only buy Baring’s stake, but also Jerry Rao’s (MphasiS’ chairman) stake. Jerry Rao is also the current chairman of Nasscom (Correction : Jerry Rao was the chairman of Nasscom till last year. For those who may not know this - N.R.Narayanamurthy of Infosys is his maternal uncle as well.). The speculation is that the discussion between EDS and MphasiS is also intended to determine how the senior management, including the founders of MphasiS, will be absorbed in EDS. Jerry Rao, the former Citibanker-turned-entrepreneur who set up the company, is expected to head the global financial services practice of EDS post merger. Currently, Jean-Louis Bravard leads EDS’ global financial services. The rationale for the acquisition is that EDS wants to ramp up its financial services practice to compete head on with IBM Global Services. EDS has been working on strengthening this practice for the last three years. IBM’s acquisition of PwC has helped it to steal a march in this domain. Now, EDS is trying to bridge that gap by acquiring MphasiS.While both EDS & Mphasis have not confirmed or denied, am not too sure of how much value would accrue to EDS by this acquisition - atleast for two reasons - key people are said to be moving out/already moved out and the valuation might be seen to be a little high.. This may also mean that more offshore companies with annual turnover less than 200 million may choose to sellout.

Yahoo! Chief Financial Officer - Susan Decker recently told Bloomberg News that Yahoo! does not intend to gain market share in the search space. "It's not our goal to be #1 in Internet search. We would be very happy to maintain our market share." (via Steve Rubel). Decker says Yahoo! will instead improve advertising on its search results pages to bring in more revenue, saying that Yahoo does not think it's reasonable to assume that it would be going to gain a lot of share from Google. She declares that, "It's not our goal to be No. 1 in Internet search. We would be very happy to maintain our market share." Yahoo!'s comments underline the difficulties any Internet company faces in trying to challenge Google's dominance of the Web search industry. Google has at least double the market share of Yahoo! and Microsoft Corp. In Internet search, the largest and most profitable segment of online advertising. To boost revenue from each search, Yahoo! plans to make ads more relevant to search terms, meaning people will be more likely to click on them.Yahoo is not moving fast enough here. On the one hand while it claims that thay are very strong in Asia , it is surprising to note that yahoo ads are not rendered if the site publisher does not have a US postal address. Google has this facility for several months!! Consider The final punch : “Our goal has been to hold our share and to be a leading, if not the leading, total marketing platform, which would include both brand and search." One can’t find fault with Yahoo : its perhaps the most sensible of the internet companies.

The year that past by was an eventful year for enterprise software vendors - small vendors finding difficult to expand and began to get acquired, the acquiring entities after spending so much on acquisition found their stocks wailing at several year lows. New technologies keep getting mindshare. 2006 appears to be another testing year for software vendors. Courtesy of Paul Kedrosky. saw this collection of perspectives on Enterprise Software. Greg Gianforte sees 2006 as the horrible year for software vendors. As he sees it,2006 will be a horrible year for software vendors who don't understand the technical and business implications of SaaS, as well as for those that remain slaves of Oracle and Microsoft. Pointing out that the issue as usual isn't just the technology itself It's whether the vendor can package and deliver the technology in a way that solves the customer's business problem and is relatively painless to assimilate into an IT environment that's already quite complex and tough to manage. He predicts that the hosted SaaS model will continue to grow, while the conventional high-TCO model will become increasingly unappetizing to corporate IT buyers who now have a great alternative. Open source will also continue its ascent as buyers realize there is no reason to pay outrageous licensing fees for proprietary operating systems, databases and web servers when the open source alternatives are just as good or better. Companies will also spend on technologies that enable them to create a superlative customer experience across all channels, since competitive success in a "flat earth" economy will depend more and more on differentiated service - rather than price and/or features. In a globalized economy, it is tough to compete on price. And with technology proliferating so quickly around the globe, it's also tough to compete on technological innovation alone. So a great customer experience has become a critical competitive differentiator. Radha Basu, CEO, President and Chairman, SupportSoft, Inc sees transition happening for enterprise software vendors. She sees the rising trend of convergence of the consumer world and the enterprise. In 2005 there has been an increased convergence in consumer-facing technologies that is forcing enterprises to re-inspect their internal software needs. Fast adoption of wireless, VoIP, high speed data access and other forms of IP-based service delivery when combined with an increasingly mobile workforce, is causing enterprises to re-evaluate how they use technology to serve themselves and their customers. Mass adoption of technology is now helping drive enterprise adoption of new solutions. For, David Gould, CEO and Chairman, Witness Systems 2006 looks favourable.

Past success may not ensure greater business this year onwards, market consolidating or not. Clearly we shall see a different landscape of enteprise software vendors when 2006 closes.

Few months back, I wrote about SOA & the potential for profound change. The article higlighted that a longstanding dream of enterprises - to define the enterprise as a set of process models - becomes possible and processes begin to take center stage in defining, configuring and running software. Software can be described using many levels of models: data elements, business objects, services and processes and SOA influences all these tiers of software. Forward looking organizations realize that these changes will have an impact on everything from development tools to methodologies of deployment, maintenance, selection and procurement cycles. Dave Chappell of DavidChappell associates points out that SOA needs to be thought in terms of : - Application architecture (Guidelines, patterns, and practices for creating service-oriented applications), - Infrastructure architecture(Guidelines, patterns, and practices for managing and operating service-oriented applications) and, - Enterprise architecture(Guidelines, patterns, and practices for using and getting business value from service-oriented applications). He adds that in general developers are mostly interested in the challenges of building service-oriented applications, for instance, and so their focus tends to be on the application architecture aspects of SOA.A vendor of web services management tools commonly thinks of SOA primarily in the infrastructure sense, while an enterprise architect at a user organization is likely to be concerned mainly with SOA’s enterprise aspects. Many people ask me where is the profound change that I talked about happening with SOA – The answer quite simply lay in working on all the three SOA dimensions. Half baked measures always produce sub-optimal results. I wrote sometime back,"For now though, SOA is a recognizable and mostly virtual plumbing exercise. Most likely, vendors will draw their strategy from the experience of customers, and will adjust accordingly. Not to overlook the fact that though the vendor community is trying hard to improve their SOA maturity,evolving standards and entrenched infrastructure mean more pilots and lab environments and more & more scope for innovations as adoption tends to improve". No wonder the SOA space is also getting consolodated as can be seen here, here & here.

The telecom landscape is getting recast and the battle is becoming one of finding sustainable ways and means of extracting value from the digital content. As we wrote the takeovers of AT&T and MCI officially usher in the long-heralded Internet era.The old phone companies are artifacts, and the new telecoms will look more like their counterparts in cable and computers. Consumers and business will increasingly have their pick of new services from a bunch of providers that are fighting hard to win their business.But as that era fades,another is dawning.The telco’s if they have their way may decide whether msn or yahoo could load faster in an user’ system.The telco’s proposals have the potential, within just a few years, to alter the flow of commerce and information - and one’s personal experience - on the Internet. For the first time, the companies that own the equipment that delivers the Internet could, for a price, give one company priority on their networks over another. The telco’s do not think that the fees imposed by carriers alter the basic nature of the Internet. No broadband provider has proposed to block certain Web sites. But they have said Yahoo, for instance, could pay a fee to have its search site load faster than Google. Other possibilities include restricting bandwidth-hogging file-swapping applications, or delivering their own video content faster than a similar service provided by rivals. SBC CEO Ed Whitecare says that the internet sites & VoIP payers would like to use my pipes free, but I ain't going to let them do that because we have spent this capital and we have to have a return on it. So there's going to have to be some mechanism for these people who use these pipes to pay for the portion they're using. The Internet can't be free in that sense, because we and the cable companies have made an investment and for a Google or Yahoo! () or Vonage or anybody to expect to use these pipes [for] free is nuts! Recently an executive with BellSouth was quoted saying that the company would consider charging Apple five or 10 cents extra each time a customer downloaded a song using iTunes. Google and others say that the prospect of telephone companies imposing new fees on innovative and successful ventures is exactly the kind of thing that deters online commerce. Cable companies abhor the idea of enforced network neutrality just as much as the telephone companies. This represents a break with the commercial meritocracy that has ruled the Internet until now. Network neutrality is increasingly becoming the buzzword that some are trying hard to have it indoctrined into law and regulation. Google and Yahoo have joined their lobbying efforts. And online retailers, Internet travel services, news media and hundreds of other companies that do business on the Web also have a lot at stake. Giving priority to a company that pays more, they say, is just offering another tier of service - like an airline offering business as well as economy class. Network neutrality, they say, is a solution in search of a problem.

I recently covered the topic of enterprise analytics. The philosophy behind business analytics had always been - mine the transaction data under your management to detect trends and extract insights that will give you competitive advantage.This only becomes more compelling with every year’s exponential expansion of the universe of accessible transaction data & the internet enablement of IT exacerbates the trend. Geoffrey Moore points out that Business analytics needs to close the loop from generating the insights to using them to drive operating procedures that can systematically capitalize upon them in time and at scale has been the exception rather than the rule.When the exception happens, the results are transforming. But for the most part we see a landscape of intermittent connections, flashes of insight, but no systemic gain. He is on the mark in pointing out that most of the business analytics engagements inside enterprises represent a highly evolved form of corporate entertainment. Its core practitioners generate insights without accountability. They communicate those insights to business managers, who do have accountability and who are moved to act, but who are unable to do so in time. As a result the insights become part of a growing library of great but lost opportunities, supporting a culture eroding into passive aggressive despair. The right answer as he sees is to grow business analytics in closed-loop systems where operationalizing the insight, making the bet, and keeping track of wins and losses, is inseparable from the generating the insight. With this firmly set in, organizations gear up to apply technology—with a mixture of brute force and finesse—to multiple business problems. Organizations shall then direct their energies toward finding the right focus, building the right culture, and hiring the right people to make optimal use of the data they constantly churn. In the end, as Tom Davenport very rightly says so, that people and strategy, as much as information technology, give such organizations strength.Most companies in most industries have excellent reasons to pursue strategies shaped by analytics.

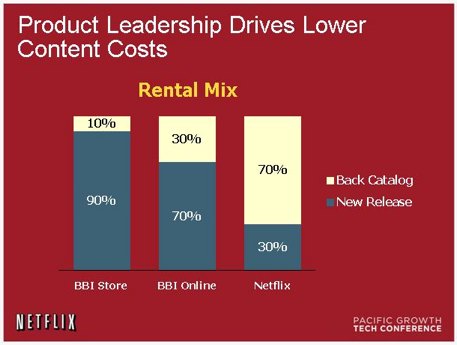

The NYTimes has an excellent article about the recommendation engines and ecommerce success. Amazon.com extensively uses collaborative filtering and association software that helps the system to make recommendations to customers based on purchase/interests shown by the customer. Web technology capable of compiling vast amounts of customer data now makes it possible for online stores to recommend items tailored to a specific shopper's interests. Companies are finding that getting those personalized recommendations right - or even close - can mean significantly higher sales. For consumers, a recommendation system can either represent a vaguely annoying invasion of privacy or a big help in bringing order to a sea of choices. Walmart.com had a toughtime when its recommendation system made wrong recommendation – all based on bruteforce matching. Wal-Mart's trouble stemmed not from the aggressive use of advanced cross-selling technology, but from the near lack of it. Companies with more nuanced strategies have avoided embarrassing linkages. NetFlix claims that roughly two-thirds of the films rented were recommended to subscribers by the site. Between 70 and 80 percent of NetFlix rentals come from the company's back catalog of 38,000 films rather than recent releases. NetFlix's recommendation system collected more than two million ratings forms from subscribers daily to add to its huge database of users' likes and dislikes. The system assigns different ratings to a movie depending on a particular subscriber's tastes. The company credits the system's ability to make automated yet accurate recommendations as a major factor in its growth from 600,000 subscribers in 2002 to nearly 4 million today. Netflix says that a key driver to their growth will be the superiority of their website design and proprietary algorithms. The personalization of their site is really what makes their service so unique. At this point Netflix has now collected over 1 billion ratings for moves. They use these ratings to make recommendations of longtail content for their consumersSimilarly, Apple's iTunes online music store features a system of recommending new music as a way of increasing customers' attachment to the site and, presumably, their purchases. Recommendation engines, which grew out of the technology used to serve up personalized ads on Web sites, now typically involve some level of "collaborative filtering" to tailor data automatically to individuals or groups of users. Liveplasma.com, an online site for music and, more recently, movies, graphically "maps" shoppers' potential interests. Interestingly technology is not the leveler here - large online stores are having success through recommendations, smaller web sites are having a more difficult time using the technology to their advantage –partly because one needs a lot of customer data to find patterns that can help in making right recommendations to customers. As I wrote earlier, heightened competition, mass usage and a variety of services all open up new range of offerings and opportunities in this increasingly felt experience economy.

We recently covered on the topic of the phenomenal increase in average productivity growth , the growth rate in the last five years in the US is seen to be the highest over the past half century. Productivity associated with offshoring is always a hot topic- given that all major enterprises are actively embracing it - this draft OECD paper assessing offshoring & productivity finds positive correation between these two - atleast in the service sectors. Technology’s contribution is not just the progress that we see in the conventional sense –it is contributing highly positively to the economy & the expectation is that it should continue to do so in future. Bweek writes about the new buzzword - "transformational outsourcing"- and suggesting that there’s a new attitude that is emerging in corporations across the U.S. and Europe in virtually every industry. A well written article starts by highlighting that the world is discovering that offshoring is really about corporate growth, making better use of skilled U.S. staff, and even job creation in the U.S., not just cheap wages abroad. The gains on labor savings pales when compared to the enormous gains in efficiency, productivity, quality, and revenues that can be achieved by fully leveraging offshore talent.The benefits can range from a chance to turn around dying businesses, speed up their pace of innovation, or fund development projects, create game changing radical business models,or help look at it as a broader plan to overhaul outdated office operations and prepare for new competitive battles. The uncorking of energy towards innovation and meeting customer needs and means to survival are all associated with benefits of offshoring. Don’t miss out reading the fact that the offshoring maturity is reaching new heights – almost akin to “Processes , on sale” The net effect : Some believe this would lead to realigning companies to deliver products faster at lower costs, and are better able to compete against anyone in the world, others theorize about the "totally disaggregated corporation," wherein every function not regarded as crucial is stripped away. Some use this to create lofty goals – P&G wants 50% of all new P&G products to come from outside by 2010, vs. 20% now. Detroit and European carmakers may go the way of the PC industry, relying on outsiders to develop new models bearing their brand names. Big Pharma will bring blockbuster drugs to market at a fraction of the current $1 billion average cost by allying with partners in molecular research and clinical testing. The rise of the offshore option is dramatically changing the economics of reengineering. Read my recent article on the emergence of disruptive models in the software industry. Clearly the winning companies of the future will be those most adept at leveraging global talent to transform themselves and their industries, creating better jobs for everyone.

Complete with graphics and well tabulated data, it’s a neat read. Do not miss out the compilation of hot players in the offshore outsourcing world( though some statistics needs update in classifying players doing above billion dollar business & also some promotions into 500millUSD club even while it may well happen several qyarters into the future (clearly unitended though - but beware - Gartner/Bweek need not be right always! - this time even in reporting public financial numbers), major players in Outsourcing, Modular corporation. The case studies of Penske & BoFA makes the reading more rich. Is it all one sided - Hardly- Look at this, relate Genpact came from the GE stable. Next time around while covering the topic - hopefully Bweek shall come with up benefits in hard numbers(these are beginning to get available) to make readers understand the impact in numerical terms much better.

Sadagopan's Weblog on Emerging Technologies, Trends,Thoughts, Ideas & Cyberworld "All views expressed are my personal views are not related in any way to my employer"